When Kellogg's Rice Krispies are toasted the cooked and dried rice "berries" expand their size (puff) to many times their normal size.

When Kellogg's Rice Krispies are toasted the cooked and dried rice "berries" expand their size (puff) to many times their normal size.Since the weight of the rice berry and its material mass remains nearly the same, the rice material is stretched to form very thin walls of the Rice Krispies structure.

This is much like a very thin glass crystal. When subjected to a change in heat, a severe "stress" is set up and the thin wall fractures - creating a Snap, Crackle and Pop!

This happens in the cereal bowl when cold milk (i.e. heat stress) is poured in the Rice Krispies and presto SNAP! CRACKLE! POP! The sounds are made by the uneven absorption of milk by the cereal bubbles.

It seems the market as of late is much like a bowl of Rice Krispies.

When subjected to a change in sentiment, severe "stress" situation are set up. Distinct SNAP! CRACKLE! POP! sounds are made by the uneven absorption of decreasing liquidity in various market bubbles. Let's take a look at a few examples.

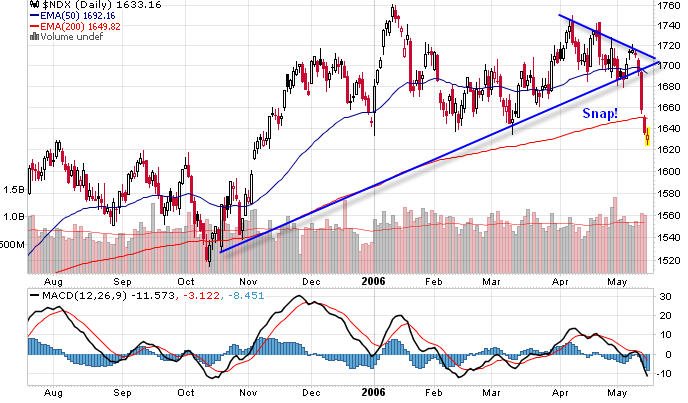

Snap!

A loud Snap! was heard when the $NDX broke both the trendline and the 200 day moving average.

The Homebuilder index snapped its trendline on a weekly basis and as you can easily see has plenty of room to fall.

Investors (using the word loosely) have been pouring into various emerging market ETFs without paying any attention to how technically stretched those charts were. TRF, the Templeton Russia ETF is one such example. In spite of a 20% snapback in a mere three days, the fund is still 21% above NAV. There are many such examples of technical damage done to charts over the last couple weeks or so, some just since last Wednesday. Is this another chance to buy or is it the start of something more significant? That of course is million dollar question.

Crackle!

The crackling sounds you are hearing can be depicted by rising foreclosures as well as the National Association of Homebuilders Housing Index. It dropped below 50% for the first time since 911. Two of the last three times it plunged like this a recession followed. There was a plunge but no recession in 1995.

MarketWatch is reporting Builders' confidence falls to 11-year low.

Contractors have negative outlook on market for first time since late 2001Traffic down, future expectations up. Sounds like denial to me.

The NAHB/Wells Fargo housing market index, a builders' sentiment gauge, fell six points in May from a revised 51 to 45, the lowest level since June 1995, the industry group said. The index shows more builders say the market is "poor" than say it's "good."

Despite the sharp decline, builders are still more optimistic about sales over the next six months than they are of current sales.

In May, builders' assessment of current single-family home sales fell to 50 from 55. The assessment of future sales dropped to 54 from 59. The assessment of traffic of prospective buyers dropped to 32 from 39. All three subindexes were at their lowest levels since mid-1995.

Expectations for sales in the next six months decreased during in May by five points to 54, the NAHB said. The traffic of prospective buyers fell the most sharply, dropping seven points to 32.

The Atlanta Journal is reporting Home foreclosures soar, with Georgia leading the way.

Georgia leads the country in the rate of foreclosure, RealtyTrac said. The number of Georgia homes in some stage of foreclosure has more than doubled since the end of 2005. Currently, there is one foreclosure for every 127 households � almost 25,000 homes statewide � RealtyTrac reported.The Coloradoan is reporting a sharp increase in foreclosures.

Rick Sharga, vice president of marketing for RealtyTrac, said recent mergers and layoffs in some of metro Atlanta's largest employers help explain the sharp rise in foreclosures. Unemployment and foreclosure rates are closely linked, Sharga said.

"That could be a factor in a place like Georgia where you've had a lot of churn," Sharga said.

The Consumer Credit Counseling Service of metro Atlanta, which works with foreclosed homeowners like Steedley, reported a 20 percent increase in first-quarter 2006 referrals for housing finance problems compared with the first quarter of 2005.

CCCS President Suzanne Boas said Georgia's short foreclosure process, which bypasses the court system, contributes to the state's high rate because it attracts aggressive lenders willing to make loans to marginal candidates. Once a property enters foreclosure, it can be sold at public auction within 37 days.

"Our state is very attractive to lenders, and part of that is our non-judicial foreclosure process," Boas said. "There have been a number of incredibly aggressive products [loans] marketed to consumers over the past five to eight years. Now we're starting to see the fallout of that aggressive marketing."

Colorado saw the second highest foreclosure ratios in the first three months of the year, a time in which nationally, foreclosures increased 38 percent over the previous quarter.WTVM is reporting forclosures in Columbus are rising

"The sharp increase in foreclosures in the first quarter continues a steady upward trend that we've seen since the beginning of the year last year," said James Saccacio, CEO of RealtyTrac.

Over-zealous homebuilding is adding supply at a rate too quick for the current market to absorb. More than one-fifth of the Larimer County households that entered foreclosure in March was a brand new home.

The supply of homes for sale on the market is another factor. Fifty percent of the homes on the market in the region are vacant, including about 20 percent which are brand new homes.

More than 13,000 Colorado households entered foreclosure proceedings during the first quarter this year, at the second-worst rate in the nation after Georgia.

Experts say foreclosures in Columbus are up 25 percent from last year. The culprit -- rising mortgage rates. Something a lot of homeowners didn't budget for.The Crackle! sound you hear is that of people buckling under the weight of a mortgage they never really could afford in the first place.

"I don't think people really read the fine print about what was going to happen to their payment when the interest rates went up,"says Daniels.

Greedy lenders made it easy for people to buy houses but difficult for people to hang on to them. This sound is only going to get louder as it spreads to states where housing prices still have not yet taken a significant tumble.

Pop!

The Pop!Pop!Pop! sound you hear is from bubble areas like Florida where speculators want out so bad they are willing to walk away from $80,000 deposits.

The National Post (Canada) is asking Housing boom a bust?

South Florida was once so hot speculators flocked to buy and flip properties. Now the market has cooled so much they're walking away from US$80,000 deposits"Never before has housing come to permeate the economic and social fabric to the extent that it does today. So that's why, if you ask me, what the No. 1 risk is to the U.S. economy: It is going to be what the house-price landscape is, what happens to house prices."

"This is the first cycle that you could actually instantaneously crystallize the rise in the notional price of a home and use it for current consumption," says David Rosenberg, chief North American economist for Merrill Lynch & Co.

"The mortgage market today is bigger than the government bond market; housing is valued at double the level of household equities on the household balance sheet," he says. "Never before has housing come to permeate the economic and social fabric to the extent that it does today. So that's why, if you ask me, what the No. 1 risk is to the U.S. economy: It is going to be what the house-price landscape is, what happens to house prices."

In Miami-Dade County alone, there are 25,000 condos under construction and another 25,000 that have already got their financing and are likely to go forward, says Jack McCabe, chief executive of McCabe Research and Consulting in Deerfield, Fla. In addition, 50,000 more have been announced.

In the whole period from 1995 to 2004, only 9,079 units were built in Miami Dade.

The Merrill Lynch study found non-traditional mortgage products accounted for 60% of loans last year in California, the hottest market in the United States.

"That's really bizarre," says Mr. Shaffer at Prestige Mortgage. "When you think about it, you should be fixing at historically low rates."

Many flippers are now walking away from their deposits or trying to wiggle out of their contracts, using shoddy workmanship as a loophole. Mr. Morgan says he now has 43 investors who are walking away from deposits of US$35,000 to US$80,000.

In Miami-Dade McCabe is reporting a potential 100,000 more condos coming online with 25,000 of them already started. No matter how you look at it, that is a bubble and it is popping now. The size of the mortgage bubble is both enormous and obvious. Well at least it should be obvious by the sounds being made.

Denial or Deaf?

Please consider Bottom's up? Maybe.

Some estimates predict a fifth of the nation�s 77 million baby boomers will buy homes in Florida in the next decade."It's a buyer's market but buyer's don't know it yet." Yeah right. It makes as much sense to say it's a sellers market but sellers don't know how to price their units to sell. Rising inventories and falling sales both show that the housing bubble has a lot more popping to do.

�Southwest Florida is still a very solid market,� said Timmerman, based in Naples. �We�ve got a lot of people with money who still like it here.�

That�s not much consolation to impatient sellers like Kasey Reavis, who now finds herself competing with thousands of other sellers in a flooded market that�s seen sales slow to a crawl.

A single mom who works for a property management company, Reavis hopes to use the money she makes off her Golden Gate house to move to a more affordable area in Georgia. She�s got her eye on a town with a good school district.

�I�m lucky if I have $30 left at the end of the week,� Reavis said.

But leaving requires a buyer.

Her three-bedroom, two-bath house with a new roof and new tile on a corner lot is listed for $299,900 � a price that was hard to find in last year�s market that saw agents fielding multiple offers for properties as soon as they hit the market. Reavis paid $150,000 in 2003.

After almost a month on the market, Reavis� agent hadn�t shown it to a single potential buyer.

It�s a lament from agents all over town these days: Where are the buyers? It�s a buyers� market, but many buyers still don�t know it.

�A lot of people have some very inflated numbers,� said Rob Dowling, a Naples agent with the John R. Wood real estate firm. �They�re saying �Gosh, if I can get all that money, I will move.��

Mish addendum: This was written two days ago and first used today by WhiskeyAndGunpowder. The index charts above will reflect that, and now look worse, a louder "Snap!" if you would.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

0 comments:

Post a Comment