U.S. mortgage applications rose for the first time in four weeks, led by a rebound in home purchase loans despite interest rates hitting their highest this year, an industry trade group said on Wednesday.I thought the jump in activity was a little surprising as well, although as Sloan says the "index can be volatile". I asked Mike Morgan at MorganFlorida if he could step outside Florida and comment on the numbers. Here was his reply:

The Mortgage Bankers Association said its seasonally adjusted index of mortgage application activity for the week ended April 28 increased 8.8 percent to 596.8 from the previous week's 548.6.

The MBA's seasonally adjusted purchase mortgage index rose 11.3 percent to 433.3 from the previous week's 389.4, which was its lowest level since November 2003.

However, the index -- considered a timely gauge of U.S. home sales -- was below its year-ago level of 482.5.

"The jump in activity was a little surprising given that mortgage rates have been rising, but on a week-to-week basis the index can be volatile," said David Sloan, senior economist at 4CAST Ltd. in New York. "Higher rates will eventually send the index lower."

A year ago most speculators did not have to close on homes. They could simply flip their contracts prior to closing. No need to apply for a mortgage. That was shut down starting about a year ago. So we actually have a double counting of mortgage applications being reported now. The flippers that never had to get a mortgage before now have to get a mortgage and close, even if they are flipping the property the same day and the new buyer has to get a mortgage. So not only are mortgage applications not realistically up, but they are substantially down. The Fed and MBA is double counting mortgage apps for those flippers that only need the mortgages to close.That is one possible explanation and a tip of the hat to Mike Morgan for explaining "flipper anomalies". A flight from ARMs is yet another reason for the recent uptick in total activity.

The builders are not selling more homes. Take out the flippers and you have a horrible decrease in �true� mortgage applications. The real year-to-year numbers will not show up for another year. There is no soft landing to this housing market. The smart money knows this and is positioning accordingly. The money that sits on the Street and does not make a trip out in the field is still star struck by the numbers based on misleading foundations.

I�ve had a few analysts and media people fly down and tour the area. Their responses have been amusing. One big analyst cut his trip short after seeing the number of houses for sale in new developments and the number of high-rise condos going up. He said he had seen enough and started calling clients on our way back to my office!

The Street needs to get out in the field and see the thousands of homes for sale in active developments, where builders are competing with the flippers that have are desperate to sell their properties. There is no way for the builders to compete with these guys, unless the builders want to slash margins by 25-35%. If they slash margins to compete, they will lose money.

The Washington Post is reporting Reasons Change for Refinancing.

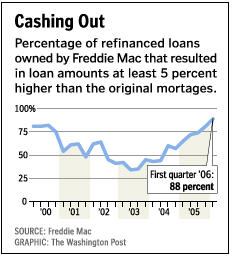

Gee do we need to add Chicken Little to Bird Sounds?A greater proportion of mortgage refinancers tapped their home equity for cash in the first three months of this year than in any other quarter in the past 15 years, according to the latest quarterly review of loans owned by Freddie Mac.

About 88 percent of people refinancing their homes took out loans for at least 5 percent more than their original balances.

The percentage of cash-out refinancings in the first quarter was the highest since the third quarter of 1990, about the time the real estate boom of the late 1980s ended, according to Freddie Mac.

In addition, more than half took loans at higher interest rates than they previously paid. In years past, refinancers chased lower rates.

Ira Rheingold, general counsel of the National Association of Consumer Advocates, said he feared that some people are spending too much of their equity, which could leave them financially exposed.

"I don't want to sound like Chicken Little here, but we're heading for a big fall," Rheingold said. "Our policy of using our homes as our banks is bad public policy, and we need to think of the long-term implications of the debt we have. It's a homeownership economy where people don't really own their homes."

Is it possible to have an ownership society where no one really owns a thing?

For the answer to those questions please consider the Methuselah of mortgages.

The Methuselah of mortgages has arrived: the 50-year home loan. Statewide Bancorp of Rancho Cucamonga began offering the loan in late March, to California residents.According to Diaz, the 50-year loan is a "lifeline" as well as "the next logical step". If that step fails what is the next logical step after that, 75-year loans to save an extra $50 a month? Mr. Diaz I think you have something ass backwards. Getting a 50-year loan is NOT a perfectly rational way to avoid an interest-only or payment-option adjustable-rate mortgage. What would be perfectly rational would be not buying a house if a 50 year loan was the only way someone could afford it. What you are peddling is "perfect rationalization" of a product that makes little practical since just so you can sell a few more loans.

Half of first-time home buyers are 32 or older, according to the National Association of Realtors. If those buyers get 50-year mortgages and never refinance or make extra payments, they won't pay off their loans until they're well into their 80s. Would they be crazy to get loans that amortize or pay off the balance over 50 years instead of the standard 30 years? Not at all, Diaz says.

Getting a 50-year loan is a perfectly rational way to avoid an interest-only or payment-option adjustable-rate mortgage, he says. "Payment-option ARMs and interest-onlies have been so popular, we wanted to come out with a longer-term, fully amortizing loan for people who don't want to go negative," Diaz says.

Regulators and consumers worry that foreclosures will surge in coming years, especially among homeowners who got interest-only and payment-option ARMs. The 50-year loan is a lifeline for them, Diaz says.

"There are two markets for this," he says. "One is if they're looking to purchase a home, because of how expensive housing is, they'll consider this loan. And the other is payment-option ARMs -- borrowers are making minimum payments and they're starting to panic a little bit and look for vehicles to get out of these loans."

About a quarter of new mortgages in California are 40-year loans. This is the next logical step, Diaz believes.

Let's do a little math shall we?

Actually I do not have to since it is right from the article. Here goes:

But just for grins, let's compare a 30-year fixed-rate loan with a mythical 50-year fixed. For a 30-year loan of $300,000 at 6.5 percent, principal and interest cost $1,896.20 per month. A 50-year loan for the same amount and at the same rate costs $1,691.15 per month in principal and interest.Does that sound like a good deal? For who? Of course most people don't plan on living in a home for 50 years. But is that a good excuse for paying nothing down and practically nothing but interest for close to the life of the loan? Actually loans like these may have the effect of trapping some people in their homes for years.

The 50-year loan costs $205 less per month, but the payments stretch out for 20 years longer and will cost a total of $332,058 more.

A housing slump will put many people underwater. Anyone in that situation would not be able to sell unless they could bring cash to the table at closing. Those are the very same people now stretching to get into houses on these new 40 and 50 year loans. Will they be trapped or will they have cash to bring to the table?

The latest numbers prove that people are still trying to live off home equity in spite of rising rates and falling home prices. "The percentage of cash-out refinancings in the first quarter was the highest since the third quarter of 1990, about the time the real estate boom of the late 1980s ended".

The hangover from this party is going to be a doozie.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

0 comments:

Post a Comment