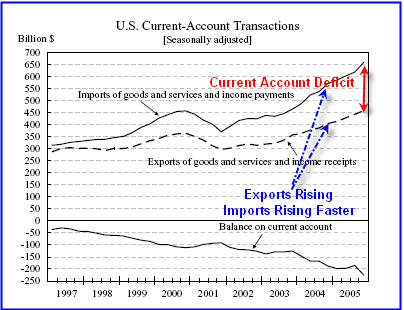

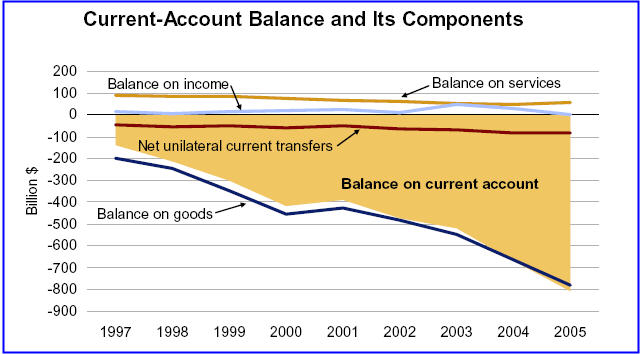

For all of 2005, the current account balance grew to a record deficit of $804.9 billion, totaling a record 6.4% of GDP.

The current account balance is a broad measure of the nation's economic balance sheet with the rest of the world. It encompasses both trade and capital flows. It essentially measures the nation's debt with the rest of the world, which must be financed by loans from abroad or asset sales to foreigners. It was the ninth annual record in the past ten years. The deficit in the third quarter was revised to a record $185.4 billion, compared with the original estimate of $195.8 billion.

Alice in Wonderland

In our current Alice in Wonderland scenario, the US (one of the richest per capita income countries in the world) is borrowing heavily from China (one of the poorest).

In Save More! Save Less! Stephen Roach had this to say Mar 09, 2006:

The two major players in the global economy, the US and China, are operating at opposite ends of the saving spectrum. Thrifty Chinese have taken saving to excess, while profligate Americans have spent their way into debt.In Tripwires on Mar 13, 2006 Stephen Roach went on to say:

Last year China saved about half of its gross domestic product, or some $1.1 trillion. At the same time, the US saved only 13% of its national income, or $1.6 trillion. That's right, the US, whose economy is six times the size of China's, can't manage to save twice as much money.

And that's just looking at national averages that include saving by consumers, businesses, and governments. The contrast is even starker at the household level � a personal saving rate in China of about 30% of household income, compared with a US rate that dipped into negative territory last year (-0.4% of after-tax household income).

These are extreme readings by any standard. The US hasn't pushed its personal saving rate this far into negative territory since 1933, in the depths of the Depression. And the Chinese rate is higher than it has been at any point in the past 28 years, since its modern reforms began. Similar extremes show up in the consumption shares of the two economies � the mirror image of trends in personal saving rates. US consumption has held at a record 71% of GDP since early 2002, while Chinese consumption appears to have slipped to a record low of about 50% of GDP in 2005.

America's lack of saving has also put unprecedented demands on the rest of the world, since the US must import surplus saving from abroad in order to grow. America's current account deficit hit a record of nearly 6.5% of GDP in 2005 and could well be headed north of 7% this year. That translates into a lifeline of foreign capital totaling about $3 billion per business day.

There is a more insidious connection between the saving postures of China and the US: Chinese savers are, in effect, subsidizing the spending binge of American consumers.

The Dubai port incident, unfortunately, is only the tip of a much bigger iceberg. There was also last year�s high-profile rejection of a bid to buy Unocal by a Chinese oil company. Moreover, in recent weeks, Washington�s increasingly xenophobic politicians have gone even further. A leading US senator floated the possibility of legislation preventing cross-border acquisitions of US companies by foreign state-owned entities. And during last week�s negotiations over the debt ceiling bill -- with a lifting of the government�s debt limit required only because a saving-short US has decided to up the ante on deficit spending -- there was actually an attempt made to restrict foreign ownership of US Treasuries. The good news, if you want to call it that, is that this latter attempt has since been watered down �only� to require a detailed accounting of the overseas holding of US government debt. But the irony of these politically motivated efforts to throw �sand in the gears� of America�s external funding mechanism is especially striking: At precisely the moment when the US has pushed its external funding requirements into unprecedented territory, it is becoming more and more aggressive in dictating the terms of the requisite inflows.Bernanke Washes His Hands

To me, all this speaks of an increasingly treacherous endgame for the current state of tranquility in world financial markets -- especially the all-important expectational underpinnings of the dollar and longer-term US real interest rates. Investors are nearly unanimous these days in dismissing the mounting economic and political tensions of an unbalanced world -- arguing that it is in everyone�s best interest to keep the game going. The retort of increasingly smug US fund managers is typically something along the lines of, �What else are the Chinese going to buy -- euros?�

Add in the current tensions associated with widening income disparities, real wage stagnation in developed countries, and the growing outbreak of trade frictions and protectionism, and today�s world looks far from secure. The tripwires of globalization are now being set.

On March 14th Ben Bernanke attempted to wash the US Government's hands as well as the FED's own hands by claiming Imbalances are driven by markets not policy.

Global trade imbalances are a market-driven phenomenon that government policies can do little to address, U.S. Federal Reserve Chairman Ben Bernanke said in a letter released on Tuesday.Quite frankly this is preposterous. The FED slashed interest rates to 1%, which spawned off a global property bubble, reignited the stock market bubble, and embarked on the greatest liquidity experiment the world has ever seen. Meanwhile the Bush administration slashed taxes, increased spending and Ben Bernanke wants us to believe that somehow this is China's fault and not US government and FED policies largely responsible for this situation?!

"In the absence of a shift in market perceptions of the relative attractiveness of U.S. and foreign assets, government policies would likely have only limited effects on the trade balance," Bernanke said in the March 9 letter to New Jersey Democratic Sen. Robert Menendez.

The letter was in response to a question the senator submitted in connection with a February 16 Senate Banking Committee hearing on the Fed's semiannual report on monetary policy. "This excess saving has been attracted to the United States by our favorable investment climate, strong productivity growth, and deep financial markets," he said.

To top it off, not only do we run enormous imbalances with the rest of the world we want to tell them what they can or can not buy with THEIR dollars. At precisely the moment when the US has pushed its external funding requirements into unprecedented territory, [the US] is becoming more and more aggressive in dictating the terms of the requisite inflows.

Last year we refused to let China buy controlling interest in Unocal , and recently refused to let the United Arab Emirates take over operations of our ports. For the record, oil is fungible and it would not have mattered one bit whether we sold Unocal to China vs. anyone else. Just Last week Congress actually had the audacity to propose restricting foreign ownership of US Treasuries (quite frankly that is laughable or scary depending on how you look at it). We also restrict "sensitive" software, military hardware, and anything else they really want.

Ben Bernanke, care for a little debate on this idea of yours that "Market Forces" and not the government that is the culprit here?

Protectionism

Does anyone believe US threats of "protectionist barriers" unless China takes action on currency reform?

Speaking on Tuesday, US Commerce Secretary Carlos Gutierrez said that if China did not take action on currency reform it would encourage those in the US seeking to put up "protectionist barriers".I am wondering if that is a credible threat. Are we really hell bent on raising prices of Chinese goods 25% to save 300 underwear manufacturing jobs in the US? Then again it could be a serious mistake to underestimate blatant stupidity on behalf of Congress in general and this Congress in particular. It will be shades of Smoot-Hawley if we pass such legislation.

Support for legislation which would slap tariffs of more than 25% on certain Chinese goods if Beijing does not further revalue the yuan is thought to be gaining support among sections of Congress. Pressure is growing for China to act ahead of a visit by Chinese president Hu Jintao to the US next month.

"If our economic relationship is to stay afloat, China needs to lighten the load by carrying out reforms and delivering results," Mr. Gutierrez said.

Quite frankly, and unfortunately there are credibility gaps of this nature everywhere you look: on the budget, on social security, on WOMDs, on Iraq, on housing, on wiretapping, on Medicaid, on homeland security, on jobs and on the war on terror. Furthermore there is a blatant bombardment of BS from both the public an private sectors.

Housing Credibility Gaps

David Lereah, the National Association of Realtors chief economist, said the latest housing reading shows a flattening that is in line with "the soft landing we've been expecting." for the housing market. "We are at a much more sustainable level of home sales now - a welcome cooling from the super-heated conditions that were driving exceptional price gains."

How can he possibly know we are experiencing a soft landing when we have not landed yet? Furthermore does anyone find his statement credible that Realtors "welcome" this cooling?

What is that saying about swampland in Florida? I think it goes something like this: "If you believe 'that' then I've got some swampland in Florida to sell you." Is that what is happening here? St. Joe Company Introduces "FloridaWild" Land Parcels of 40 Acres and More, Ideal for Outdoor Enthusiasts and Conservationists.

Ideal? Ideal for what? Wading in muck and getting attacked by swarms of mosquitoes?

I think there is a serious credibility issue here.

Snow is Confident

Back on March 3rd treasury Secretary Snow said the Failure to save shows confidence in future paychecks.

In a telephone interview with The Chronicle, Snow said that he thinks wages now are at a "tipping point" where they will start rising. Snow also put a positive spin on Americans' negative savings rate. Recent studies have shown that in 2005 average spending outpaced earnings for the first time since 1933 as people financed consumption by dipping into savings or taking on debt.Does anyone really find that credible? If so, I've got some swampland in Florida to sell you.

"One way to look at it is that people tend to consume out of their expected long-term income," he said. "The strong consumption could be interpreted, probably should be interpreted, as a vote of confidence in the direction of the economy and the fact that people feel good about their prospective earnings, the sustainability of their jobs and the strength of the job markets."

Bernanke Praises Derivatives

On March 15 Ben Bernanke was quoted as saying Derivatives make economy resilient

"Although no single factor accounts for this favorable performance, derivative instruments undoubtedly have contributed to this resilience because they offer firms means for managing their risks," Bernanke said.On March 15 Bloomberg reported Credit Derivatives Market Expands to $17.3 Trillion.

His comment was in response to a question submitted in writing from Republican Sen. Mike Crapo of Idaho in connection with a February 16 Senate Banking Committee hearing on the Fed's semiannual report on monetary policy.

Bernanke said derivatives, whose value is based on that of some underlying factor, "have contributed to our understanding of the measurement and management of risk" and thus helped make the financial system as a whole more resistant to shocks.

"Certainly, derivatives instruments pose challenges to risk managers and to supervisors, but these risks are manageable and thus far have been managed quite well," Bernanke said.

"Market discipline has provided strong incentives for effective risk management, the key to ensuring that the benefits of derivatives continue to be realized," he added.

The global market for credit derivatives increased by 39 percent to $17.3 trillion in the second half of 2005 on demand for contracts to bet on corporate credit quality or insure against defaults, the International Swaps and Derivatives Association said.The other side of the Derivative Debate

Credit-default swaps, which pay compensation in the event of borrowers defaulting on their debt, expanded 105 percent in the full year, leading an increase in the $236-trillion market for derivatives, or contracts based on underlying assets. The market's growth was slower than 123 percent increase in 2004, ISDA said in a report today at its annual meeting in Singapore.

Regulators are worried that credit derivatives are increasing too quickly for banks to control. The Federal Reserve Bank of New York has demanded action to tackle a backlog of contracts left unsigned for weeks or months, and for banks to address a shortage of bonds to settle contracts.

Contracts to swap between fixed and floating interest payments, the biggest derivatives market, increased 6 percent to $213.2 trillion, ISDA said. The growth rate was slower than the 10 percent expansion in the first half, said New York-based ISDA, a trade group representing more than 700 banks, securities firms and institutional investors.

Back on March 7th, Howard Simmons (one of my favorite contributors to RealMoney.com) wrote an interesting piece entitled Dana Bonds Show Ugly Credit Incentive . Following are a few snips:

One of the sadder and more predictable outgrowths of the expansion of the Federal Savings and Loan Insurance Corp. (FSLIC) insurance in 1980 to $100,000 per account was the emergence of the "Texas Run" toward troubled S&Ls. That's right, toward. As word spread that an S&L was in trouble, it was forced to pay a higher rate on its certificates of deposit. CD brokers, not to be confused with homonymous seedy brokers, bundled all sorts of small deposits into $100,000 packages and sent them to the troubled S&L. Who cared if the S&L then failed? The CDs were insured.So we have a world where 14,000% to 17,500% of the total bonds of a corporation are in play via credit derivatives and this according to Bernanke "makes the economy resilient"? Is infinite leverage is a good thing? It must be according to Bernanke.

Credit Default Insurance

The topic of credit default swaps (CDS) and how they are used was outlined here last April and then again in May. These instruments act as put options; they allow the bondholder to deliver the bonds at par, the bond's face value, to the CDS writer in the event of a credit event. As the risk of bankruptcy or another credit event rises, the price of a CDS expressed in basis points rises as well. CDS writers, like those who write put options, are on the hook to buy the bonds at par to deliver to the CDS buyers.

Just as the open interest of a futures or options contract can swell to a quantity greater than what is available for delivery, the volume of CDS contracts created in this over-the-counter market can swell way beyond the physical quantity of the actual corporate bonds being covered. And I do mean way beyond; while actual data are hard to come by, some estimate that the volume of outstanding CDS contracts on bonds for now-bankrupt auto parts manufacturer Delphi was 140 to 175 times the actual quantity of bonds available.

The world of distressed-security hedge funds and the emergence of credit traders have created a situation wherein the bondholder gets rewarded when the company gets in trouble. Every corporate bond with an excess of CDS written on it now embeds a call option on the firm's bankruptcy. Once a firm gets into trouble and blood is in the water, the bondholders may have a positive incentive to see the firm fail.

Yes, insurance changes behavior. Free stock options created problems in the 1990s boom. Will these "free" call options on bankruptcy create incentives among the bondholders, especially those who hold CDS protection, to see the firm fail? Absolutely, and the sooner we address this issue, the fewer next-generation Enrons and WorldComs we will see.

Ben Bernanke ($Ben) has long ago blown his credibility. Every time he opens his mouth the credibility gap seems to widen. I apologize for not posting a chart of the combined total credibility gap. It simply went off the scale.

Notes:

There is an audio covering this blog and much more on Howe Street.

Please look in the left hand column for "Startling stats and a Credibility Gap" by Mike 'Mish' Shedlock. In the past, some people have reported problems playing those podcasts. I think most of the problems have been solved, even for Apple users. Please play that podcast and let me know of any problems you are experiencing, and I will pass them on to HoweStreet.

I am also pleased to announce that I am starting a newsletter called the "Survival Report" with a good friend, Brian McAuley, a superb chart technician. For more details please subscribe to Whiskey & Gunpowder, a free publication. The current edition is available for free at The Survival Report. Brian and I welcome your feedback and your suggestions.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

0 comments:

Post a Comment