That of course is a far cry from the world but to that you can add in a huge property bust in China that is now underway as well as a stagnant Europe (many countries) that never really got going. Europe borders on deflation and a global slowdown just might do them in. You might also consider how a slowdown in US consumer purchases will affect the world. With that thought, let's get started.

Forbes is reporting a big slump in New Zealand business confidence.

Business confidence in New Zealand has slumped to its lowest level since 1986 as nation's economic growth slows, according to the New Zealand Institute of Economic Research (NZIER) quarterly survey of business opinionUS 4th Quarter GDP 2.7% annualized

The institute said the December quarter survey suggests the economy is currently in the throes of a potentially acute slowdown

While inflation is likely to hover near the top of the Reserve Bank of New Zealand's target band of 1-3 pct annual CPI inflation or marginally above it for some time, NZIER said it believes the survey results suggest the central bank can afford to hold and then gradually loosen monetary policy during 2006 and into 2007

It said slowing domestic demand will reduce underlying inflationary pressure while further interest rate rises will exacerbate the sharpness of a downturn which is already very clearly underway

In December the Reserve Bank of New Zealand raised its official cash rate 25 basis points to 7.25 pct in an attempt to slow domestic demand and maintain the rate at the highest level among industrialized nations

Last month, NZIER said New Zealand's economic growth is likely to slow to 2.3 pct in the current year to March 2006 from 3.6 pct a year earlier, as business activity slows and domestic demand eases following two years of rising interest rates The December quarter survey showed a net 61 pct of firms expect business conditions to deteriorate over the next six months compared with 32 pct in the previous survey

Seasonally adjusted, a net 71 pct of firms are despondent compared with 34 pct in the September survey

NZIER said the sizable increase in negative sentiment in the December quarter occurred throughout all regions and all industry groups with manufacturers the most pessimistic.

MarketWatch is reporting the U.S. economy slows to below trend.

The U.S. economy grew at the slowest pace in nearly three years in the just-concluded fourth quarter, economists estimate.Let's dissect some quotes from that article.

Led by what could be the weakest consumer spending since 1991, the economy likely grew at about a 2.7% annual pace in the fourth quarter after 11 straight quarters of growth above 3%, economists say.

The slowdown is just what the Federal Reserve wants at this point in the business cycle. The Fed has boosted its short-term interest rate target 13 times since mid-2004 in a bid to put the brakes on the economy.

Above-trend growth has been sopping up excess capacity in the economy and leading to shortages and bottlenecks that can fuel inflation.

The Fed is expected to raise rates again on Jan. 31 and likely in March.

Few economists expect the slump to worsen significantly. For the first quarter, economists are estimating growth at 3.6%, approximately the economy's long-term potential. Most economists do see growth slowing again at the end of the year as the housing market weakens.

"The economy could get back to an above-trend rate this quarter, and that is what will matter to monetary policy makers," said Joseph LaVorgna, chief U.S. fixed income economist for Deutsche Bank.

While most economists had forecast a modest slowing in the fourth quarter, it looks as if the slump was worse than expected. At the beginning of the quarter, economists were expecting growth of about 3.2%.

Consumer spending, business investment and government spending all underperformed relative to expectations. The collapse of auto sales likely subtracted a full percentage from growth, UBS economists said.

Housing was one of the few bright spots in the fourth quarter's growth mix, along with inventory rebuilding.

"We do not believe the apparent weakness in the fourth quarter represents a clear change in the trend," said James O'Sullivan, an economist for UBS. GDP will likely slow from about 3.6% in 2005 to 3% in 2006 and 2.7% in 2007, he said.

The course of consumer spending this year is very much an open question. Some economists, such as Ian Shepherdson of High Frequency Economics, believe a sharp slowdown in housing later this year will force consumers to rein in their spending.

It's possible that consumer spending outpaced consumer's disposable incomes in 2006 for the first time since the Great Depression.

Paul Kasriel, top economist for Northern Trust, figures that $2.5 trillion of outstanding household debt will reprice at a higher interest rate this year, forcing households to devote more of their paycheck to servicing their mortgage and credit card bills.

But other economists say consumer spending will be fine this year. Household income growth should be strong enough to maintain healthy spending.

"We expect consumer spending growth to remain solid this year even as the housing market slows," said Dean Maki, economist with Barclays Capital. Most of the wealth that households extracted from their home equity was used to pay down more expensive debt, not to fund current consumption, Maki said. That would make consumer spending less vulnerable if home prices fall.

"Household income growth should 'remain' strong".

The reality is that wage growth as well as job growth have both been dramatically below par throughout this entire recovery.

"Housing was one of the few bright spots in the fourth quarter's growth mix".

Seriously, where do they get this stuff? Enquiring Mish readers want to know.

No Pricing Power in the UK

Please take a look at the UK where output prices fell for 3rd straight month, the first time since Aug 2001.

Manufacturers continued to find it difficult to pass on increases in their raw material costs during December, official figures showed today.Input prices were up 17.2% but there was no ability to pass on price increases.

Even though the annual rise in input prices during the month was the highest since records began in 1991, the office for National Statistics revealed that output prices fell for the third consecutive month for the first time since August 2001.

Between November and December, output prices, on a non-adjusted basis, fell by 0.2 pct. Although the fall was less than the previous month's 0.3 pct, analysts had actually predicted a 0.1 pct increase.

The subdued monthly output prices may come as a surprise to some analysts and officials at the Bank of England because of another increase in input prices, which rose 0.9 pct in December from November on a seasonally adjusted, just shy of analysts' expectations of a 1.0 pct.

On a year-on-year basis, input prices were up 17.2 pct, higher than analysts' expectations of a 15.7 pct increase. The December rise was the highest since records began in 1991.

Fancy that. It's a possibility only diehard deflationists would consider possible.

Record numbers call debt advisers after Christmas

The Guardian is reporting Britain cuts back on credit card habit.

Visa data shows shoppers switching to debit cards.Property Bubbles Popping

Record numbers call debt advisers after Christmas.

This indicates that consumers are taking on board warnings about running up too much debt. Instead, shoppers are using their debit cards for their spending.

The data from the card group coincided with news of a surge in the number of calls to debt advice lines during the first two weeks of the year as borrowers took stock after Christmas.

Meanwhile, record numbers of people were calling debt advisory services after finding they were struggling to pay back what they owe. The Consumer Credit Counselling Service took 9,310 calls in the first nine working days of the year - up almost 14% on the same period in 2005.

National Debtline also reported huge demand, receiving almost 13,000 calls between January 3 and lunchtime on Friday. The organisation admitted that the surge in demand had left it struggling to cope, with about two thirds of its calls going unanswered, although it said most people did get through on subsequent attempts.

It said it was in the process of recruiting 25 additional staff to add to the 55 employees who currently answer its phones in an attempt to meet the demand.

If you missed the housing situation in China, you may wish to read:

Shanghai Housing Bubble Pops.

I also suggest watching Centex "One Day" Sales to see if they really are for "one day" only.

I doubt it.

You might wish to check out this report on San Diego housing. It came out today.

The Union Tribune is reporting House resales take a tumble in December.

San Diego County resale house prices tumbled last month by the biggest number in 18 years of record-keeping and contributed to the smallest year-to-year rise in overall prices in six years, DataQuick Information Systems reported Monday.Summary

The median resale price for existing single-family homes dropped $15,000 from November to December to stand at $550,000, the largest month-to-month decline since DataQuick began keeping records in 1988.

Last year was the first time since 2001 that the number of home sales fell from the previous year. The total sold last year was 55,366, down 9.1 percent from 2004's 60,886. Monthly sales reports from DataQuick have showed a decline in activity on a year-over-year basis for 18 straight months.

On Thursday, the San Diego Association of Realtors, which monitors about 60 percent of the housing market, reported that properties took longer to sell in 2005 than in 2004 � lingering on the market for, on average, 62 days last year compared to 54 in 2004.

The total number of listings has been growing, reaching a peak of just over 15,000 listings in November, about five times more than at the peak of the buying frenzy in spring 2004.

- 4th Quarter US GDP was 2.7%, a dramatic slowdown likely to continue

- No pricing power in the UK in spite of massive rise in PPI

- A Property bust in China

- A Property bust beginning in the US, and spreading dramatically

- Trichet very cautious on EU hikes as Europe lagged the world

- Europe is just too little too late to fuel the world economy

- Record numbers calling debt advisors after Christmas

Mish update: The above text was written on January 16th and previously appeared in

Whiskey and Gunpowder and HoweStreet.

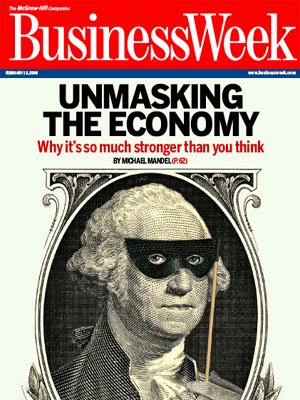

Further proof that the top is in just arrived with this BusinessWeek cover Unmasking The Economy.

Why The Economy Is A Lot Stronger Than You Think

In a knowledge-based world, the traditional measures don't tell the story. Intangibles like R&D are tracked poorly, if at all. Factor them in and everything changes.

In a knowledge-based world, traditional measures don't tell the story! Sheeesh. I wonder what Warren Buffet might think about that. This is just another version of "It's different this time". Haven't we had enough of that already?

There is nothing like magazine covers espousing some new economic nonsense to mark the top. The BusinessWeek cover is perfect.

I congratulated Time Magazine back in June for calling the top in the real estate with this silly cover.

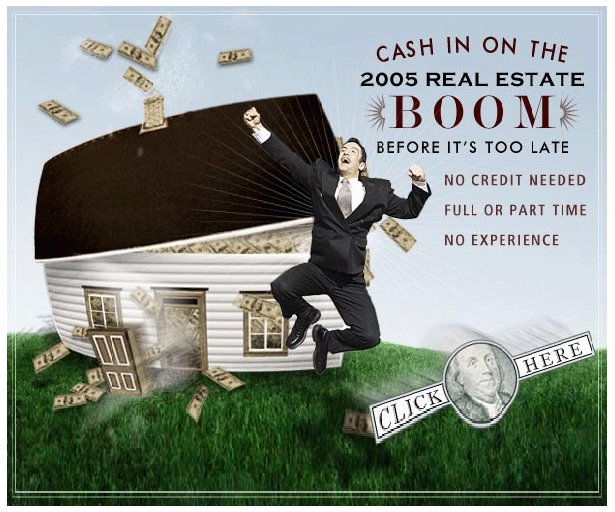

I reported "It's Too Late" immediately after I received this Email ad:

The economy is about to be unmasked alright. It will be exposed for the house of cards that it is, completely dependent on creative financing and worsening credit lending standards, consumer debt, negative savings, and home equity extraction from houses expected to rise in price forever.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

0 comments:

Post a Comment