:: Contemporary Art Museum St. Louis, St. LouisAs always, at The Archi-Tourist contributors and contributions are always welcome!

:: The Pulitzer Foundation for the Arts, St. Louis

:: Chaussegros-de-Lery Complex, Montreal

:: Cite Multimedia 7, Montreal

:: Cite Multimedia 8, Montreal

:: Cirque du Soleil Dormitory, Montreal

Sunday, April 30, 2006

Archi-Tourist Updates

Prompted by my friend Frank's post at Metroblogging Montreal, and the realization that I've grown slack with any additions the site, I added a bunch of entries to The Archi-Tourist over the weekend.

Saturday, April 29, 2006

Panic Over Oil

Sometimes I am nearly speechless over dumb ideas coming from this Congress. This is one of those times. Please consider the CNN article Senators to push for $100 gas rebate checks.

The Democrats were inspired alright, inspired to come up with their own silly plan.

Democrats Propose 60-day Moratorium on Gasoline Tax.

Free Money

Now I am all in favor of lower taxes, but I am also in favor of lower spending. Neither plan comes close but the Republican plan seems like it is from Mars. Is there a fiscal conservative Republican anywhere to be found? Other than Ron Paul, who? When I first read the idea of free $100 bills I thought I was reading something from "The Onion".

How can anyone possibly think that "free money" can be given away with no repercussions? What planet are our senators and congressman from anyway? Isn't the national debt big enough already? If not, why stop at $100. Heck why not give every citizen in the country $100,000? That would buy a lot of gas. Or would it? Perhaps gas would go to $150 a gallon or more if they did that. Who knows? All I know is that there is no such thing as free money.

Strategic Oil Reserves Halted

Bloomberg is reporting Bush Halts Oil Reserve Deposits, Plans Fuel Waivers

Ethanol Tax Credits and Tariffs

There are currently tax credits of 51 cents per gallon for suppliers and an extra 10 cent per gallon tax credit to provide extra help to small ethanol producers and farmers. If it takes 61 cents in tax credits to make something profitable for corn growers then that is 61 cents in tax credits not wisely spent. All Congress is doing is wasting taxpayer money by buying votes.

This should be proof enough: Brazil Finance Minister Asks US To End Ethanol Tariff.

By the way, Chris Puplava on FinancialSense produced some great charts in an article entitled ENERGY ECONOMICS 101 that make a mockery of gouging claims.

Breakup Oil Firms Proposal

Is that the end of dumb ideas coming from Congress about oil? By now, Mish readers know the answer to questions like that automatically: "of course not". Please consider a proposal by senator Charles Schumer (D-NY) to breakup oil firms.

What is gold telling us?

On April 25th, Ron Paul, perhaps the only person in Congress with any clues gave a congressional speech about What the Price of Gold is Telling Us. Following are the key snips in a very lengthy article.

Compare and contrast the fiscal sanity and wisdom of Ron Paul with the idea of giving every citizen $100 "free money" to help counteract rising gas prices.

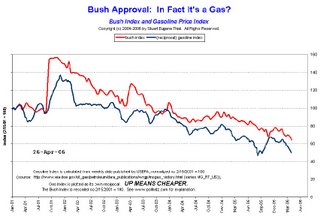

It seems to me Bush and the Republican Congress and practically everyone else except for Ron Paul is in a panic over oil. Perhaps the following chart with thanks to Professor Pollkatz, just might explain why. For a much larger and easier to read gif file please click here.

The reason we are in such dire fiscal straights is there are too many politicians with their hands in the till, too many politicians that see nothing wrong with buying votes, too many politicians that do not understand what inflation really is, and quite frankly too many jackasses running the country counterbalanced by one Ron Paul whom everyone ignores.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Most American taxpayers would get $100 rebate checks to offset the pain of higher pump prices for gasoline, under an amendment Senate Republicans hope to bring to a vote soon. "Our plan would give taxpayers a hundred dollar gas tax holiday rebate check to help ease the pain that they're feeling at the pump," Senate Majority Leader Bill Frist announced Thursday.Gas Tax Moratorium

"It also includes strong federal anti-price gouging protection to protect consumers against anti-competitive behavior by oil companies or other suppliers of gasoline. Our free market system works, but it works best when there's full accountability and full transparency."

Frist said the rebates would go to single taxpayers making less than $125,000 per year, and couples making less than $150,000.

Republican senators said they hoped soaring gas prices would inspire Democrats to support their proposals.

The Democrats were inspired alright, inspired to come up with their own silly plan.

Democrats Propose 60-day Moratorium on Gasoline Tax.

Following President Bush's four-point plan outlined today, Democrats proposed legislation that would put a moratorium on the Federal gasoline tax for at least 60-days to provide consumers immediate relief at the pump. But the proposed legislation would also chop oil company tax benefits and burden refineries with unwarranted reporting requirements, making it unable to win enough support in Congress to have even a remote chance of passing.On the whole, the Republican plan is far dumber. But both plans want government to investigate "price gouging". Let's be serious here. Is there any evidence of price gouging? How much are we going to waste trying to determine if there is price gouging? Heck, why not give the contract to Halliburton?

For years, Democrats have been fighting to get tough on Big Oil and protect Americans from being exploited when they fuel their cars," said Senate Democratic Leader "give em hell Harry" Reid. "Unfortunately, for years Republicans have been more interested in protecting oil companies' profits than the American people's pockets. Now that gas prices are skyrocketing and Americans are struggling just to fill their gas tanks, Congress must act to ease the burden. Passing a federal gas tax holiday and repealing the tax giveaways in the Bush energy bill is a good start."

The Menendez Federal Gas Tax Holiday Amendment, an amendment to the Supplemental Appropriations Bill under debate in the U.S. Senate right now, will give Americans immediate relief from gas prices right at the pump by removing the $0.184 per gallon federal tax on gasoline and the $0.244 per gallon federal tax on diesel for 60 days. To recover the lost revenue, the amendment repeals huge and unnecessary subsidies for large oil companies included in the Bush energy bill and other legislation and handed out at a time when oil companies were enjoying record profits.

"More than six months ago, Democrats, led by Congressman Bart Stupak of Michigan, introduced legislation that gives the Federal Trade Commission (FTC) explicit authority to investigate and prosecute companies engaged in price gouging. Congressional Republicans voted three times against acting on this Stupak legislation.

"Democrats, led by Congressman Brian Higgins of New York, introduced a bill that would rescind billions of dollars in taxpayer subsidies for these oil companies, roll back these subsidies, tax breaks, and royalty relief given to big oil and big gas companies, and use those funds to help low-income Americans, farms, and small-businesses struggling under the weight of gas prices. And yes, the Republicans voted over and over against rolling back the subsidies even after they knew the oil companies were making historic, obscene, and record profits.

Free Money

Now I am all in favor of lower taxes, but I am also in favor of lower spending. Neither plan comes close but the Republican plan seems like it is from Mars. Is there a fiscal conservative Republican anywhere to be found? Other than Ron Paul, who? When I first read the idea of free $100 bills I thought I was reading something from "The Onion".

How can anyone possibly think that "free money" can be given away with no repercussions? What planet are our senators and congressman from anyway? Isn't the national debt big enough already? If not, why stop at $100. Heck why not give every citizen in the country $100,000? That would buy a lot of gas. Or would it? Perhaps gas would go to $150 a gallon or more if they did that. Who knows? All I know is that there is no such thing as free money.

Strategic Oil Reserves Halted

Bloomberg is reporting Bush Halts Oil Reserve Deposits, Plans Fuel Waivers

President George W. Bush, facing voter concern over soaring fuel prices, said he will free up oil that is being added to the nation's emergency reserves and waive rules that are creating bottlenecks in U.S. gasoline markets.Let's do a quick calculation. We import 10,000,000 barrels a day of which 25,000 goes to the strategic reserves. My math says that will help by 1/4 of 1%. In other words, Bush is touting something that is statistically irrelevant.

Bush, in a speech today in Washington to the trade group for ethanol producers, said the country should raise fuel efficiency and develop alternatives to oil. He also ordered the Justice Department to look for possible price manipulation.

"We'll leave a little more oil on the market" by halting deliveries to the reserves, Bush said. "Every little bit helps."

Bush and Republicans in Congress face growing pressure from voters as crude oil soars to a record and gasoline pump prices near the all-time high reached after Hurricane Katrina last year. A CNN poll released yesterday showed 69 percent of U.S. adults say higher fuel costs are causing financial hardship.

The Energy Department will suspend deposits to the Strategic Petroleum Reserve through the end of summer, which is the period of peak demand in the U.S., Bush said.

Because the stockpile is nearly full, the effect of the halt may be minimal. The government has been adding an average of about 25,000 barrels of oil per day to the reserve so far this year. The U.S. imports about 10 million barrels a day.

"The first thing to do is to make sure Americans are treated fairly at the gas pump," Bush said. "This administration is not going to tolerate manipulation."

Boone Pickens, the Dallas hedge fund manager and a Bush supporter, said he was disappointed that Bush is talking about investigations.

"There's not anything there. There's not anybody gouging," Pickens said in an interview today at the Milken Institute conference in Los Angeles. "You have the Federal Trade Commission looking at gasoline prices every day."

Ethanol Tax Credits and Tariffs

There are currently tax credits of 51 cents per gallon for suppliers and an extra 10 cent per gallon tax credit to provide extra help to small ethanol producers and farmers. If it takes 61 cents in tax credits to make something profitable for corn growers then that is 61 cents in tax credits not wisely spent. All Congress is doing is wasting taxpayer money by buying votes.

This should be proof enough: Brazil Finance Minister Asks US To End Ethanol Tariff.

Brazil's Finance Minister Guido Mantega asked the U.S. government to reconsider a tariff on imports of ethanol from Brazil, the Valor newspaper said Monday.Here we are supposedly struggling to lower gas prices and a non-opec country wants to supply us with cheaper ethanol than we can produce it, and this administration says "no thanks". Instead we worry about non-existent price gouging. Go figure.

The U.S. currently slaps a tariff of $0.54 per gallon on Brazilian ethanol, mainly to protect domestic producers of the alternative fuel, who produce it far more expensively than Brazilians. But U.S. farmers are having difficulties keeping up with rising demand as refiners are substituting the gasoline additive MTBE with ethanol.

The tariff "is worse for the U.S. itself, as it makes the ethanol the country needs more expensive," Mantega is quoted as saying.

In a presentation, Mantega said that Brazilian ethanol currently had a cost of about $20 a barrel and that the fuel is an important piece in the search for cleaner energy sources.

By the way, Chris Puplava on FinancialSense produced some great charts in an article entitled ENERGY ECONOMICS 101 that make a mockery of gouging claims.

Breakup Oil Firms Proposal

Is that the end of dumb ideas coming from Congress about oil? By now, Mish readers know the answer to questions like that automatically: "of course not". Please consider a proposal by senator Charles Schumer (D-NY) to breakup oil firms.

"We also have to reexamine whether having only a handful of giant oil companies can coexist with the needs of the American consumer and a rational energy policy in this country -- I do not believe it does," Schumer declared. "And so I'll be offering an amendment to the supplemental that will require a complete examination as to whether or not we should break up the big oil companies."How long ago was it that we broke up "Ma Bell" only to allow it to be put back together piece by piece? Was anything accomplished? If so what?

"Enough is enough," the New York senator added. "We have no competition. There are signs of it. I've talked to business leaders who buy oil and gas products, major, conservative Republican business leaders, and they don't believe the market is on the level."

�If $75 a barrel, $3 a gallon isn't a wake-up call to this country, then what is?

�And prices are going to continue to go up. If we do nothing, we'll look back at the days when it was $3 a gallon, and say, "Boy, that was a lot better than it is today."

�So we need to do three things -- and we are pushing for three things in the real security package that the House and Senate leadership -- Democratic leadership on both sides -- have put together.

�First, we have to dramatically increase conservation. We're not doing any of that. The fact that China has higher mileage standards than we do should make us weep. And China is not a country caring about the environment -- they're doing it just to keep their economic strength.

What is gold telling us?

On April 25th, Ron Paul, perhaps the only person in Congress with any clues gave a congressional speech about What the Price of Gold is Telling Us. Following are the key snips in a very lengthy article.

Since 2001 however, interest in gold has soared along with its price. With the price now over $600 an ounce, a lot more people are becoming interested in gold as an investment and an economic indicator. Much can be learned by understanding what the rising dollar price of gold means.Panic Time

The rise in gold prices from $250 per ounce in 2001 to over $600 today has drawn investors and speculators into the precious metals market. Though many already have made handsome profits, buying gold per se should not be touted as a good investment. After all, gold earns no interest and its quality never changes. It�s static, and does not grow as sound investments should.

It�s more accurate to say that one might invest in a gold or silver mining company, where management, labor costs, and the nature of new discoveries all play a vital role in determining the quality of the investment and the profits made.

Buying gold and holding it is somewhat analogous to converting one�s savings into one hundred dollar bills and hiding them under the mattress-- yet not exactly the same. Both gold and dollars are considered money, and holding money does not qualify as an investment. There�s a big difference between the two however, since by holding paper money one loses purchasing power. The purchasing power of commodity money, i.e. gold, however, goes up if the government devalues the circulating fiat currency.

One of the characteristics of commodity money-- one that originated naturally in the marketplace-- is that it must serve as a store of value. Gold and silver meet that test-- paper does not. Because of this profound difference, the incentive and wisdom of holding emergency funds in the form of gold becomes attractive when the official currency is being devalued. It�s more attractive than trying to save wealth in the form of a fiat currency, even when earning some nominal interest. The lack of earned interest on gold is not a problem once people realize the purchasing power of their currency is declining faster than the interest rates they might earn. The purchasing power of gold can rise even faster than increases in the cost of living.

The point is that most who buy gold do so to protect against a depreciating currency rather than as an investment in the classical sense. Americans understand this less than citizens of other countries; some nations have suffered from severe monetary inflation that literally led to the destruction of their national currency. Though our inflation-- i.e. the depreciation of the U.S. dollar-- has been insidious, average Americans are unaware of how this occurs. For instance, few Americans know nor seem concerned that the 1913 pre-Federal Reserve dollar is now worth only four cents. Officially, our central bankers and our politicians express no fear that the course on which we are set is fraught with great danger to our economy and our political system. The belief that money created out of thin air can work economic miracles, if only properly �managed,� is pervasive in D.C.

In many ways we shouldn�t be surprised about this trust in such an unsound system. For at least four generations our government-run universities have systematically preached a monetary doctrine justifying the so-called wisdom of paper money over the �foolishness� of sound money. Not only that, paper money has worked surprisingly well in the past 35 years-- the years the world has accepted pure paper money as currency. Alan Greenspan bragged that central bankers in these several decades have gained the knowledge necessary to make paper money respond as if it were gold. This removes the problem of obtaining gold to back currency, and hence frees politicians from the rigid discipline a gold standard imposes.

The number of dollars created by the Federal Reserve, and through the fractional reserve banking system, is crucial in determining how the market assesses the relationship of the dollar and gold. Though there�s a strong correlation, it�s not instantaneous or perfectly predictable. There are many variables to consider, but in the long term the dollar price of gold represents past inflation of the money supply. Equally important, it represents the anticipation of how much new money will be created in the future. This introduces the factor of trust and confidence in our monetary authorities and our politicians. And these days the American people are casting a vote of �no confidence� in this regard, and for good reasons.

The incentive for central bankers to create new money out of thin air is twofold. One is to practice central economic planning through the manipulation of interest rates. The second is to monetize the escalating federal debt politicians create and thrive on.

Today no one in Washington believes for a minute that runaway deficits are going to be curtailed. In March alone, the federal government created an historic $85 billion deficit. The current supplemental bill going through Congress has grown from $92 billion to over $106 billion, and everyone knows it will not draw President Bush�s first veto.

Current policy guarantees that the integrity of the dollar will be undermined. Exactly when this will occur, and the extent of the resulting damage to financial system, cannot be known for sure-- but it is coming. There are plenty of indications already on the horizon.

Foreign policy plays a significant role in the economy and the value of the dollar. A foreign policy of militarism and empire building cannot be supported through direct taxation. The American people would never tolerate the taxes required to pay immediately for overseas wars, under the discipline of a gold standard. Borrowing and creating new money is much more politically palatable. It hides and delays the real costs of war, and the people are lulled into complacency-- especially since the wars we fight are couched in terms of patriotism, spreading the ideas of freedom, and stamping out terrorism. Unnecessary wars and fiat currencies go hand-in-hand, while a gold standard encourages a sensible foreign policy.

It�s a mistake to blame high gasoline and oil prices on price gouging. If we impose new taxes or fix prices, while ignoring monetary inflation, corporate subsidies, and excessive regulations, shortages will result. The market is the only way to determine the best price for any commodity. The law of supply and demand cannot be repealed. The real problems arise when government planners give subsidies to energy companies and favor one form of energy over another.

Energy prices are rising for many reasons: Inflation; increased demand from China and India; decreased supply resulting from our invasion of Iraq; anticipated disruption of supply as we push regime change in Iran; regulatory restrictions on gasoline production; government interference in the free market development of alternative fuels; and subsidies to big oil such as free leases and grants for research and development.

Meaning of the Gold Price-- Summation

A recent headline in the financial press announced that gold prices surged over concern that confrontation with Iran will further push oil prices higher. This may well reflect the current situation, but higher gold prices mainly reflect monetary expansion by the Federal Reserve. Dwelling on current events and their effect on gold prices reflects concern for symptoms rather than an understanding of the actual cause of these price increases. Without an enormous increase in the money supply over the past 35 years and a worldwide paper monetary system, this increase in the price of gold would not have occurred.

Economic law dictates reform at some point. But should we wait until the dollar is 1/1,000 of an ounce of gold or 1/2,000 of an ounce of gold? The longer we wait, the more people suffer and the more difficult reforms become. Runaway inflation inevitably leads to political chaos, something numerous countries have suffered throughout the 20th century. The worst example of course was the German inflation of the 1920s that led to the rise of Hitler. Even the communist takeover of China was associated with runaway inflation brought on by Chinese Nationalists. The time for action is now, and it is up to the American people and the U.S. Congress to demand it.

Compare and contrast the fiscal sanity and wisdom of Ron Paul with the idea of giving every citizen $100 "free money" to help counteract rising gas prices.

It seems to me Bush and the Republican Congress and practically everyone else except for Ron Paul is in a panic over oil. Perhaps the following chart with thanks to Professor Pollkatz, just might explain why. For a much larger and easier to read gif file please click here.

The reason we are in such dire fiscal straights is there are too many politicians with their hands in the till, too many politicians that see nothing wrong with buying votes, too many politicians that do not understand what inflation really is, and quite frankly too many jackasses running the country counterbalanced by one Ron Paul whom everyone ignores.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Friday, April 28, 2006

Look Who's Hiring

The Office for Metropolitan Architecture (OMA) is a leading international partnership practicing contemporary architecture, urbanism and cultural analysis.And my favorite sentence in their job post at Archinect (my emphasis):

Candidates must be highly creative, innovative and must feel confident in a complex, stressful and chaotic context.At least they're honest.

Cranes

One of the clearest signs of a thriving economy, progress, and all that comes with that is cranes. After the Berlin Wall fell and buildings started to fill the gaps in the bombed-out city, a skyline of cranes was the most prominent image for the place.

Image from here

Now, that distinction of "crane capital" would probably go to Dubai or China. Regarding the latter, I heard today that more than half of all cranes in the world currently reside on construction sites in China, an amazing fact (if true) though not necessarily surprising.

There seems to be some strange appeal for cranes, evidenced by the web page Crane Porn and an article in today's Chicago Tribune that focuses on a crane operator for Trump Tower. The graphic below is a handy guide to that tower crane (click it for the larger view with annotations).

Crane Links:

Image from here

Now, that distinction of "crane capital" would probably go to Dubai or China. Regarding the latter, I heard today that more than half of all cranes in the world currently reside on construction sites in China, an amazing fact (if true) though not necessarily surprising.

There seems to be some strange appeal for cranes, evidenced by the web page Crane Porn and an article in today's Chicago Tribune that focuses on a crane operator for Trump Tower. The graphic below is a handy guide to that tower crane (click it for the larger view with annotations).

Crane Links:

:: Crane Porn

:: Crane Porn Flickr Pool

:: Wikipedia page

:: FreeFoto.com

Strong 1st Quarter GDP Growth

Reuters is reporting GDP growth strongest in 2-1/2 years.

Then again, I suppose it could be different this time. The one thing that remains to be seen is how much more money Congress and this administration is willing to waste to keep Republicans in control of the House and Senate.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

The U.S. economy grew at its strongest rate in 2-1/2 years during the first three months of this year, snapping back from a lackluster fourth quarter on a surge in spending and investment, a Commerce Department report on Friday showed.Is anyone aware of how much consumer spending has been tied to housing gains? Has anyone looked at falling real wages, the negative savings rate, falling home sales, or rising home inventories?

Gross domestic product grew at a 4.8 percent annual rate in the January-March first quarter, more than twice the 1.7 percent rate in the fourth quarter and the strongest for any three months since 7.2 percent in the third quarter of 2003. The first-quarter figure was only slightly below the 4.9 percent rate that Wall Street economists had forecast.

The pace of price rises declined from the fourth quarter. A gauge of personal spending excluding food and energy - a measure favored by the Federal Reserve - advanced at a 2 percent rate in the first quarter compared with 2.4 percent in the fourth quarter last year.

First-quarter GDP performance was boosted by increased government spending on reconstruction in the wake of last year's devastating hurricanes on the Gulf Coast. Federal government spending shot up at a 10.8 percent rate, a sharp contrast to the 2.6 percent rate of decline in the fourth quarter. It was the strongest government spending since a 22.1 percent jump in the second quarter of 2003.

[So the solution to our problems is more hurricanes and goverment spending? Exactly what are we getting for our money? Mish]

Federal Reserve Chairman Ben Bernanke told the Joint Economic Committee on Thursday that growth was likely to moderate as the year wears on, partly because of some softness in housing markets. He also indicated that U.S. central bank policy-makers might pause fairly soon in a campaign of steady rate rises, which have brought 15 interest-rate hikes since mid-2004.

Businesses robustly boosted their investment during the first quarter, with spending rising at a 14.3 percent annual rate. That was three times the 4.5 percent fourth-quarter increase and was the largest in nearly six years, since a 14.8 percent climb in the second quarter of 2000.

[And does anyone recall exactly what happened in the third Quarter of 2000? Mish]

Spending on equipment and software alone increased at a 16.4 percent rate in the first quarter - the strongest in six years - after a 5 percent fourth-quarter rise. The strong spending implies that corporations remain optimistic about their sales prospects and are willing to make the investments to expand their businesses.

[Ya gotta love it. After 15 freaking rate hikes corporations have turned more optimistic just as we are headed for a recession - Mish]

With demand strong, inventories grew at a slower rate in the first quarter. Stocks of unsold goods increased at a $21.9 billion rate, down from $37.9 billion in the final three months last year, leaving room for factories to keep churning out more goods as long as spending remains hearty.

[As long as spending remains hearty huh? - Mish]

Then again, I suppose it could be different this time. The one thing that remains to be seen is how much more money Congress and this administration is willing to waste to keep Republicans in control of the House and Senate.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Cramer Leaving

According to the Chicago Tribune,

(Thanks to Sally for the head's up!)

On a side note, it's annoying to see Blair Kamin ending his all-too-brief report linked above with the sentence, "He also was a vocal supporter of the Soldier Field renovation." Back in 2004, Kamin anticipated Soldier Field's loss of landmark status, a position he's been pushing for quite a while. As Lynn Becker points out, "Kamin...made the new Soldier Field his own Baby Richard, filling up column after column of derisive critiques even after all doubt that the project would be built had been removed."

So even after landmark status has been dropped, the issue isn't apparently dead for Kamin. It's almost like he must mention Soldier Field in every damn column that he writes, be it appropriate or not, in this case not.

Ned Cramer, the first full-time curator at the Chicago Architecture Foundation, is leaving the non-profit group known for its tours and other programs to become editor of a planned architecture magazine in Washington, the foundation says.In his nearly four-year tenure as curator, Cramer has brought many interesting exhibitions to the CAF, including the Big & Green show on sustainable architecture and the current one on public space.

(Thanks to Sally for the head's up!)

On a side note, it's annoying to see Blair Kamin ending his all-too-brief report linked above with the sentence, "He also was a vocal supporter of the Soldier Field renovation." Back in 2004, Kamin anticipated Soldier Field's loss of landmark status, a position he's been pushing for quite a while. As Lynn Becker points out, "Kamin...made the new Soldier Field his own Baby Richard, filling up column after column of derisive critiques even after all doubt that the project would be built had been removed."

So even after landmark status has been dropped, the issue isn't apparently dead for Kamin. It's almost like he must mention Soldier Field in every damn column that he writes, be it appropriate or not, in this case not.

Thursday, April 27, 2006

New Gold Standard

Sorry gold bugs this is not what you think. David Lereah, Chief Economist of the National Association of Realtors made a claim this morning that real estate is the "new gold standard."

I just received that message along with these notes from Mike Morgan taken at a meeting today where David Lereah spoke. Following are Mike Morgan's notes and comments:

Not to worry, Real Estate is "The New Gold Standard". Besides, as everyone knows �If you have a healthy local economy it is almost impossible to have a bubble burst!� Excuse me but isn't everyone saying how healthy the economy is right now?

On one hand we see that there are �No signs of a bubble bursting.� Yet we see builders "caught with their pants down" even though bubble bursting is "almost impossible". Compare and contrast "We made a mistake. It�s going to hurt. You are going to have a double digit drop� with �2006 will be the best year ever.� Read back over Mike Morgan's notes and you will quickly see that David Lereah is talking out of both sides of his mouth at the same time, each side saying the opposite thing.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

I just received that message along with these notes from Mike Morgan taken at a meeting today where David Lereah spoke. Following are Mike Morgan's notes and comments:

Hello Everyone,OK, let's do the math as Mike suggests. 60,000 condos selling at 2,500 per year. Hmmm. It seems we have a 24 year supply of Florida condos coming online. OK let's double the sales rate to 5,000 and have the number built at the same time. 30,000 / 5,000 is a 6 year supply.

I just left a meeting where the Chief Economist of the National Association of Realtors (NAR) spoke. You all should have been there to hear his spin on the real estate market. Here are some highlights.

David Lereah was not as positive as he has been. After a few worn out jokes, he made an effort to put a positive spin on the markets. However, his wrap up summed it all up. �Some builders will get caught with their pants down, because they built too much�

He lead off by stating, the media is responsible as they are not looking at the data or putting it in the right place. I disagree emphatically. I believe the media is being conservative, as no one is looking at what these numbers are made up or where they come from. The recent release by NAR showing an increase in homes sales is a perfect example. With the Florida market being the largest component of this number, and Florida down 22%, there is no possible way to be up . . . without a footnote. There is a possibility we are seeing a spike in those folks in the Gulf Coast that lost their homes, buying new homes or renting the available inventory and forcing other market participants to buy versus rent. However, it is highly unlikely that the other States that make up the South could have boosted the numbers into positive territory . . . unless the sampling NAR does was in non-representative markets. Even with the Gulf Coast effect, that is temporary.

Mr. Lereah went on to blame the issues on FNMA making it easier to finance a home and, get this, the Internet making it easier for buyers to find homes.

Lereah noted that 40% of homes are second homes. He failed to note that most investors purchased homes and told the builders that these were primary homes. If they admitted they were second homes or investments, the builders would have either told them to walk or charged them 20% deposits. I can verify this, as many of my clients did this. Why? The home builders� sales reps told us this was the way around the investment restrictions!

He continued to paint a rosy picture by stating that real estate was the, and I quote, �new gold standard.� That�s scary, as this has been the complete opposite. If we want to analogize this market for the last few years, let�s analogize it to options, derivatives, naked puts and the Big Wheel in Vegas.

On the flip side of the rosy picture he admitted, �Prices got a �little� too high, we got ahead of ourselves. . . . We need to catch our breath.�

He then noted, �It happened in the stock market. How many people purchased Qualcomm, Lucent, I doubled down on Lucent. We became irrational during the stock market craze.� Well, I ask, how does that balance with his statement about real estate, �There were lotteries to get into deals. I got into one!� He got into one? The Chief Economist of NAR?

A few more quotes, �Go to Miami to see the excess.�

�40% of all loans in 2006 were interest only. . . Prices went higher because of the artificial energy in the real estate market . . . that�s what took the punch bowl out of the party.� Party? Did he admit this was nothing more than a party? He sure did.

After his Miami reference he said, �Naples Florida is even worse. Misery loves company.�

�We are transitioning to a buyers market. It could be 1 month, 6 months, 12 months.� Very highly unlikely that this is one month or even six months.

�If you have a healthy local economy it is almost impossible to have a bubble burst!� Well, I got news for you, we don�t have a healthy economy with oil at $75 a barrel and the bulk of all jobs created during the last few years in real estate!

�You have a great future in real estate, but you need to cleanse your real estate markets. We made a mistake. It�s going to hurt. You are going to have a double digit drop. Expect it.� And in his very next breath, �2006 will be the best year ever.�

�No signs of a bubble bursting.�

Next breath, �Naples right now is experiencing some problems.�

�Conventional wisdom turned on its head.�

I love this one. �The laws of supply and demand have not been revoked.� Exactly. We have a supply that can be analogized to Dutch tulips.

�Is this a bad year. Yes. Your numbers will down. You got ahead of yourselves. The market got ahead of itself.�

Lereah said it will be the �middle of 2007 when you start to pick up again. I see Florida picking up in 2007. But there are particular markets that will not. It depends on inventory levels.�

I guess I must ask how 60,000 condos in Miami with a 2,500 a year absorption rate isn�t a supply and demand problem. Let�s take the 60,000 reported by McCabe Research and cut it in half, and then double the absorption rate. So we have 30,000 condos and 5,000 sales. Do the numbers.

I have warned my investor clients for more than a year that this was coming. If builders, banks and real estate agents acted responsibly we would not be in this situation. Many agents blast me for being so negative and �single handedly bringing down the market.� I take great pride in how I have conducted my business. Unfortunately, I will still take quite a bit of heat, as I recommend to my clients to rent for 6-12 months and then buy . . . unless there is some overpowering reason for them to buy now. That�s certainly not what my fellow Brokers want to hear, but my duty is to my clients. As a licensed professional, I must adhere to our Code of Ethics. I do what is best for my clients, not my fellow Brokers.

Great Day to You All,

Mike

Not to worry, Real Estate is "The New Gold Standard". Besides, as everyone knows �If you have a healthy local economy it is almost impossible to have a bubble burst!� Excuse me but isn't everyone saying how healthy the economy is right now?

On one hand we see that there are �No signs of a bubble bursting.� Yet we see builders "caught with their pants down" even though bubble bursting is "almost impossible". Compare and contrast "We made a mistake. It�s going to hurt. You are going to have a double digit drop� with �2006 will be the best year ever.� Read back over Mike Morgan's notes and you will quickly see that David Lereah is talking out of both sides of his mouth at the same time, each side saying the opposite thing.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

McCabe Research April 2006

I had an interesting one hour conversation today with Jack McCabe of McCabe Research and Consulting, a firm specializing in micro/macro research of multifamily residential and commercial mixed use projects. It seems he found me after I put a double "black mark" on his soul and jokingly banned him from The Apologists Club on March 24th.

"That is a trend, not a blip," said Jack McCabe, chief executive of McCabe Research and Consulting in Deerfield Beach, adding that too many good people took out too many bad loans.

I was pleasantly greeted with a surprise phone call from him just today. I will try and summarize the conversation as best as I can. Here goes:

For starters, Jack McCabe was telling me that there are 290,000 real estate agents in Florida. "That equates to one out of every 57 people", he said. Imagine that. The real question I asked McCabe is "How many of them depend on sales commissions for their livelihood?" Let's face it I said, there are a lot of housewives masquerading as real estate professionals happy to get a sale or two a year as extra income. Jack estimated there are approximately 130,000 full time professionals based on the number of registered Florida association of realtors.

For the sake of argument let's call it 150,000 (assuming that there are some full time agents not registered with the association and others even if not full time very dependent on commissions for living expenses). That would make it roughly one in a hundred people in Florida are directly dependent on real estate for their livelihood. "But wait" Jack said, "That does not count loan originators, home builders, contractors, subcontractors, landscapers, or anything else housing related".

Jack is correct of course, and even though the others may not "need" the extra money, it is certainly flowing through the system. That is a theme I have been harping about for months as Mish readers know full well. As long as the building continues, people will have jobs. When it dies, it will be lights out.

"Look at Countrywide" McCabe said. "Countrywide?" I asked. It seems that with little fanfare Countrywide closed a South Florida office in December. With it perhaps a couple hundred people lost their jobs. "Not only that but Washington Mutual is laying off people", he said. A couple of hundred people might not sound like many, but the real question is how many home sales did a couple of hundred loan originators support?

Jack was telling me about "mezzanine financing". I had to ask him what that meant. It seems a lot of home builders were on short term financing, hoping to get projects completed "Wham bam thank you mam". Jack is now telling me that some of those developers now have a "cash flow problem". It is one thing when people are camping out overnight to get in line to buy a condo. It is a far different situation when projects are being delayed and even cancelled.

In fact, projects are now being cancelled left and right. McCabe told me of a development that has sold 2 units out of 250 after cancellations. Hello world! If that is a small time developer, that person has just been busted big time for speeding. The next step is bankruptcy.

Jack spoke of a project in Sarasota where because of a technical delay in condo document filing with the state of Florida, the developer had to recently do a special two week rescission period. Well guess what? It seems that 100 units that the developer thought were sold have now been cancelled. That is 100 out of 270! Given that not all of the units were presold, the cancellation rate is enormous. "Speculators are bailing every chance they get" he said.

I have one more interesting factoid. Jack is telling me that "as soon as ground is broken, the ability of investors to get back deposits is limited". I commented that seems like fertile ground for fraud. "Indeed", he said. It seems there are situations right now where developers are bringing in bulldozers and breaking ground "with no real intention" of getting underway with actual development. The reason they are doing this is because as soon as ground breaks at least a portion of deposits are not refundable. Some lawsuits are now underway.

Although McCabe Research specializes in Florida and the Southeast US, Jack is telling me of similar stories elsewhere including Las Vegas, San Diego, Chicago, Boston, New York, and Los Angeles. Interestingly enough, he thinks that housing is a "local problem". That was the good news. The bad news is that the "local problem" includes areas where a huge percentage of the population lives.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

"That is a trend, not a blip," said Jack McCabe, chief executive of McCabe Research and Consulting in Deerfield Beach, adding that too many good people took out too many bad loans.

I was pleasantly greeted with a surprise phone call from him just today. I will try and summarize the conversation as best as I can. Here goes:

For starters, Jack McCabe was telling me that there are 290,000 real estate agents in Florida. "That equates to one out of every 57 people", he said. Imagine that. The real question I asked McCabe is "How many of them depend on sales commissions for their livelihood?" Let's face it I said, there are a lot of housewives masquerading as real estate professionals happy to get a sale or two a year as extra income. Jack estimated there are approximately 130,000 full time professionals based on the number of registered Florida association of realtors.

For the sake of argument let's call it 150,000 (assuming that there are some full time agents not registered with the association and others even if not full time very dependent on commissions for living expenses). That would make it roughly one in a hundred people in Florida are directly dependent on real estate for their livelihood. "But wait" Jack said, "That does not count loan originators, home builders, contractors, subcontractors, landscapers, or anything else housing related".

Jack is correct of course, and even though the others may not "need" the extra money, it is certainly flowing through the system. That is a theme I have been harping about for months as Mish readers know full well. As long as the building continues, people will have jobs. When it dies, it will be lights out.

"Look at Countrywide" McCabe said. "Countrywide?" I asked. It seems that with little fanfare Countrywide closed a South Florida office in December. With it perhaps a couple hundred people lost their jobs. "Not only that but Washington Mutual is laying off people", he said. A couple of hundred people might not sound like many, but the real question is how many home sales did a couple of hundred loan originators support?

Jack was telling me about "mezzanine financing". I had to ask him what that meant. It seems a lot of home builders were on short term financing, hoping to get projects completed "Wham bam thank you mam". Jack is now telling me that some of those developers now have a "cash flow problem". It is one thing when people are camping out overnight to get in line to buy a condo. It is a far different situation when projects are being delayed and even cancelled.

In fact, projects are now being cancelled left and right. McCabe told me of a development that has sold 2 units out of 250 after cancellations. Hello world! If that is a small time developer, that person has just been busted big time for speeding. The next step is bankruptcy.

Jack spoke of a project in Sarasota where because of a technical delay in condo document filing with the state of Florida, the developer had to recently do a special two week rescission period. Well guess what? It seems that 100 units that the developer thought were sold have now been cancelled. That is 100 out of 270! Given that not all of the units were presold, the cancellation rate is enormous. "Speculators are bailing every chance they get" he said.

I have one more interesting factoid. Jack is telling me that "as soon as ground is broken, the ability of investors to get back deposits is limited". I commented that seems like fertile ground for fraud. "Indeed", he said. It seems there are situations right now where developers are bringing in bulldozers and breaking ground "with no real intention" of getting underway with actual development. The reason they are doing this is because as soon as ground breaks at least a portion of deposits are not refundable. Some lawsuits are now underway.

Although McCabe Research specializes in Florida and the Southeast US, Jack is telling me of similar stories elsewhere including Las Vegas, San Diego, Chicago, Boston, New York, and Los Angeles. Interestingly enough, he thinks that housing is a "local problem". That was the good news. The bad news is that the "local problem" includes areas where a huge percentage of the population lives.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Wednesday, April 26, 2006

Jacobs Block

Lisa Chamberlain at Polis, teaming up with Curbed, has started a contest to "Nominate the Best Jane Jacobs Block in NYC". She explains that "the idea is to celebrate the 'street ballet' of your favorite block...because it exhibits the characteristics that Jane Jacobs enumerated as essential ingredients to a quality urban life," ingredients she enumerates in her post.

I would probably submit what's above, but I don't meet the guidelines (I only have the one photo). Regardless, I'll explain what I like about it and how it meets the essential ingredients.

The block is at the intersection of MacDougal and King Streets in Soho; the photo is taken from 12 Chairs, a great little cafe that expanded in the last couple years. As you can maybe see by the photo, MacDougal is a thru-street while King Street ends in a T-intersection at MacDougal, a very rare situation in Manhattan. This condition is part of what makes this block of MacDougal (from Houston on the north to Prince on the south) so appealing: it's reduced traffic, it's mixture of two short streets, and the surprise of the T-intersection. Personally, I just love sitting in the cafe and staring out the window, a la the image above.

Like a lot of blocks in the area, it fits the four Jacobsonian ingredients that Lisa mentions:

I would probably submit what's above, but I don't meet the guidelines (I only have the one photo). Regardless, I'll explain what I like about it and how it meets the essential ingredients.

The block is at the intersection of MacDougal and King Streets in Soho; the photo is taken from 12 Chairs, a great little cafe that expanded in the last couple years. As you can maybe see by the photo, MacDougal is a thru-street while King Street ends in a T-intersection at MacDougal, a very rare situation in Manhattan. This condition is part of what makes this block of MacDougal (from Houston on the north to Prince on the south) so appealing: it's reduced traffic, it's mixture of two short streets, and the surprise of the T-intersection. Personally, I just love sitting in the cafe and staring out the window, a la the image above.

Like a lot of blocks in the area, it fits the four Jacobsonian ingredients that Lisa mentions:

1-Mixed primary uses: Retail and apartments, with a little business space as well.Visit Polis and Curbed for more information. Contest ends Friday, May 12.

2-Short blocks: Two short blocks, as noted.

3-Old Buildings: The buildings here are old yet unexceptional, perhaps making them a bit more affordable in what's an extra-expensive area.

4-High density: Party wall buildings are all along these blocks (though there might have been a vacant lot or two in the past, I can't recall and am 1,000 miles away at the moment).

Exit Stage Left

I am in nostalgia mode. Perhaps it shows my age, but I can not help but think about that loveable pink lion "Snagglepuss".

I am in nostalgia mode. Perhaps it shows my age, but I can not help but think about that loveable pink lion "Snagglepuss".After reading this post you may want to order the snagglepuss refrigerator magnet shown on the left. If so, I certainly can understand.

Enquiring minds can also preview a brief audio of "Exit Stage Left" here (The audio is free).

Before I could even ask, the telepathic thought lines were flooded with calls. "Mish what does Snagglepuss's "Exit Stage Left" have to do with the economy?

"Heavens To Murgatroid" I am pleased to announce that staging exits has once again taken center stage. Of course I have proof. Here it is:

Home Staging Tips

Barbara Corcoran has Tips for Staging Your Home. Now she does not say if it is an exit stage left or an exit stage right but she does say that "Simple Changes May Translate to Big Bucks". Let's take a look:

If you're selling your house, you should probably be staging it.The question I have is "Should it take a 'guru' to figure that out? I mean seriously, how can one take plain common sense and put a "staging" label on it? I think Snagglepuss had more common sense. Whenever Snagglepuss was in trouble he exited "Stage Left" although on rare occasions he did exit "Stage Right". Whether left or right, it should now be clear that the stages are being exited, sometimes by auction and somtimes by bankruptcy or other liquidation.

"It's always best to your put your best foot forward in any situation, and this is a way for your house to put its best foot forward," said real estate guru Barbara Corcoran.

Fixing up your home, or "staging" it, as the real estate business calls it, can raise your selling price anywhere from five to 20 percent, Corcoran says.

Here are her tips for staging your house.

Clean your house. A filthy bathroom is the worst, second only to a dirty kitchen.

Let the light in. Wash your windows, because dirty windows keep out light. And open the shades. Basically, people like light, so if your rooms have dark colors, you might want to consider repainting them.

De-clutter your house. Clutter makes your house look small and unloved.

Take a whiff. If your house has an odor, that's a huge turnoff. Make it smell nice. You might need an air filter.

Fix up the bathroom. First of all, make sure it's clean. Then, see how you can spruce it up. At the very least, re-caulk any areas that are falling apart.

Examine your front door. That's the first thing people will see. Does it need a coat of fresh paint?

Send your pets to grandma's house. A barking dog is unwelcoming. Plus, people might be allergic to yor pets.

Bargain Basement Prices

The Palm Beach Post is reporting Bargain Basement Auction Prices.

Luxe properties go for bargain at Tesoro auction.Trademark the Obvious

The gavel slammed down almost as soon as the bidding had started. In minutes. As fast as the words could tumble out of the mouth of the auctioneer, whose voice buzzed like a bumblebee: Sold for $165,000.

"We're in the basement, folks," the auctioneer said. "What a bargain."

Promising "prices we have not seen in years," auction organizers said the sea of sellers looking to unload properties was anything but a poor reflection of the Tesoro communities.

It seems "StagedHomes" is now a trademarked name.

The way you live in a home and the way you sell it are two different things. That's the premise of "Staging", a hot new trend that�s sweeping the country. In any real estate market, Staged Homes sell faster or sell for more money or both! In Home Staging, readers learn how to play up a home�s strong points and improve its presentation. This book helps readers look at their houses through the buyer�s eyes. From repairing a broken step and clearing out the clutter to trimming those overgrown bushes and painting a room, Home Staging shows readers how to play up a home�s strengths and minimize its weaknesses.Plan "B"

Not all of our modern day Snagglepusses staged an exit at the right time.

Please consider They had a plan, then reality intruded.

A group of friends who set out to buy, fix up and "flip" a Palm Springs tract house haven't found the riches they were seeking. Four friends thought they could 'flip' a house, but cost overruns, bad timing got in the way.Ah yes, the infamous "Plan B". They could not sell it for a profit in six months, pray tell what makes them think they can rent it in another six months? Even if they can, how long will all four of them be happy about the carrying costs? The good side is that those costs are now split four ways. But what is going to happen in those situations where one person is holding six mortgages hoping to flip them? If you think that scenario is not realistic then please check out 6 PROPERTIES, SELLER WILLING TO HOLD FINANCING

In August, the four bought a three-bedroom, two-bathroom, 1,900-square-foot home that seemed like a good-enough deal at $425,000. Houses in Palm Springs had been appreciating consistently, and other homes on the same street were listed for considerably more. The plan was to spend $60,000 fixing up the house, then sell it in two months for about $650,000. According to Haughey's calculations, the profit would be $60,000 after all expenses, taxes and commissions, or $15,000 for each partner.

Spirits were high when the project began. The friends worked full time during the week and then spent weekends in Palm Springs on their project. They visited tile stores, drove around neighborhoods looking at paint colors, dined at their favorite local restaurants and generally enjoyed their time together.

But as the renovation went forward, the budget crept up to $67,000, mainly because the kitchen and bathrooms cost more than expected. The kitchen got a luxury makeover with oak cabinets, some with frosted glass doors, plus brushed aluminum hardware and granite counters.

The house went on the market in early November. [It's now April and there is still no sale]. The house is now listed for $629,000, and if it sells for that, each partner will pocket just $5,000.

"It's not risk-free," Nina Smith said of her first foray into speculative remodeling. "I need to better educate myself on finding a better property."

And if the house doesn't sell for the current price?

"We have all discussed Plan B," Scalero said. "The possibility of turning it into a vacation rental. We've been told that weekly rentals go for around $1,500."

I am an investor selling the following properties. I am willing to hold financing so you can buy with no money down and in some cases, I am willing to stay on, FREE OF CHARGE, to continue to manage the existing tenants.

That poor guy wants to "Exit Stage Left" but the doors are now closed both left and right. Nationwide, the stage doors are getting tighter and tighter with every uptick in rates. Fewer and fewer speculators will be able to make it safely through the exit doors.

Mish note: The above appeared in a recent issue of Whiskey and Gunpowder. Since then I have come across more examples of staging and exits. Here goes:

Even home builders are into staging. Toll Brothers is staging easter egg hunts and refrigerator doors.

A refrigerator magnet in a Toll Brothers home may have a message to a fictitious family member about a relative that has to be picked up at a train station, demonstrating that mass transit is nearby. Or, a school jersey hung in a bedroom of the model home serves as a reminder of a good school district.George Pintye, a real estate agent in Hernando County Florida just sent me this nifty exit strategy by insurance companies: Strapped insurers flee coastal areas.

In addition to personal notes and school jerseys, Toll Brothers' marketing involves staging Easter egg hunts, Halloween parades as well as charity events or PTA meetings � another reminder of a neighborhood's school system � within a development.

With the 2006 hurricane season starting in just five weeks, many home insurers from Texas to Florida to New York are canceling policies along the coast or refusing to sell new ones out of fear of another catastrophic storm.Following are George Pintye's comments:

In the widest insurance retreat from coastal property since Hurricane Andrew slammed Florida in 1992, insurers as far north as Long Island, N.Y., and Cape Cod, Mass., are shedding coastal homeowners policies to reduce their exposure.

In Florida alone, insurers that are undercapitalized or fearful of losses have notified the state of plans to cancel more than 500,000 homeowners policies. With $2 trillion each in coastal property, Florida and New York lead the USA in coastal exposure, followed by Texas and Massachusetts.

Companies including Allstate, the USA's second-biggest property insurer, say forecasts of more major hurricanes combined with soaring coastal real estate development have created unacceptable risk in some areas.

Last year's hurricanes cost insurers a record $60 billion in claims payouts. Now Allstate, which paid out a record $5 billion in hurricane claims last year, is canceling 95,000 policies in Florida and 28,000 in New York.

�Florida. Amid mass policy cancellations, state officials are declaring a crisis. Because mortgage lenders require home insurance, affected policyholders must find other insurance, probably at higher cost. Near the coast, annual premiums of several thousand dollars now rival a mortgage's cost. Florida's state-run insurer of last resort, which must provide insurance if no other company will, has a record 815,000 policies and a $1.7 billion deficit. At the urging of state Chief Financial Officer Tom Gallagher, a judge Tuesday began placing Florida's No. 3 home insurer, Poe Financial, into receivership because it lacks adequate reserves.

�Texas. Allstate just announced it won't write any new homeowners policies in 14 coastal Texas counties. Texas' insurer of last resort, the Texas Windstorm Insurance Association, has only $1.2 billion in cash and reserves going into the new hurricane season. The association wants to raise rates 19% on homes and 24% on businesses.

�New York. Allstate says it won't write any new homeowners policies in New York City, Long Island or Westchester County. Although Long Island hasn't been struck by a major hurricane since 1938, "The probability exists for New York to be hit," says Trevino. MetLife also is cutting back on new homeowners policies near the coast. New York's legislature is considering a bill to create a permanent, state-run insurer of last resort to provide wind and fire insurance for coastal homes.

Hi Mike,Let's finish up with one of the worst stage exits in history. Play the video and I am sure you will agree. Just don't let it happen to you.

USA today has basically sounded the death knell for the Florida real estate market:

I still can't get my head around the 500,000 figure. And now, the State's # 3 insurer is going into receivership? Wonderful.

And need I mention that we've recently lost buyers (even one deal at the closing table) because of the outrageous premiums required for homeowner's insurance?

Its painful to think about what's going to happen to Florida this summer, much more as a homeowner and resident then a real esate agent.

Best Regards,

George

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

FAR vs NAR

Following is an update from Mike Morgan about the discrepancy between Florida Association of Realtors (FAR) numbers vs the National Association of Realtor (NAR) numbers:

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Several of you have called to find out why yesterday�s Florida numbers are at the opposite end of the spectrum from the National Association of Realtor (NAR) numbers. Here�s what one analyst told me after he investigated a similar disconnect prior to this one.Last Friday Mike wrote:

NAR extrapolates. They survey 1-2% of the market and then multiply and add a �fudge� factor. He said he believes they intentionally avoid distressed markets like Miami, Naples, Vegas, Phoenix, DC, etc. There goal, as our Trade Association, is to promote the industry, not to report a comprehensive picture. If they avoid the hard hit markets, their numbers will consistently paint a much better picture than what reality is.

I have not been able to confirm this, but he is a top analyst with a top securities firm. He was able to speak directly with the right people at NAR.

What he says makes perfect sense when Florida shows a 22 and 23 percent drop in homes/condos, while NAR claim the numbers are actually up. From ground zero, I can tell you, without any question whatsoever, sales are down at least 25%. Folks . . . that�s being conservative. Moreover, listings to sales are in a runaway mode. I have stopped taking listings unless the client wants to pay a nonrefundable advance fee.

The other issue that is being ignored is what goes into Existing Home Sales. Many of these homes are flippers selling their homes that they just closed on as New Home Sales. It is not a normal number. As the flippers are being forced out of the market and walking away from contracts, we will eventually see the Existing Home Sales numbers fall substantially. However, NAR can simply avoid the markets they want to avoid, and simply use data from markets that will produce a �happy� number, as he notes.

The weekly numbers I report in regard to listings to sales are direct from our MLS system. These numbers track what FAR just reported. As my Grandpa once said, �Liars can figure, but figures can�t lie.�

Engle is cranking it up a notch with a 25% boost to commissions to a lofty of 5%. A year ago the builders were paying 2% on average. Not only that, but they�re reducing prices $10,000 and giving away $15,000 in upgrades. It will be interesting to see where this all stops. Personally, I think we will see a lot of projects put on hold and a lot of condo projects failing.Hmmm Let's see. Following is the second condo bankruptcy fiasco that I have seen lately. Condo construction halted; lender files for bankruptcy.

When a Las Vegas lender plunked down money from retirees, investors and even a medical research firm's pension fund to finance construction of a West Palm Beach high-rise condo, everyone gambled that red-hot Florida real estate was a sure thing.Expect to see a lot more horror stories like that one. 50,000 condo units are coming online (or plan to) in the next couple years. That is close to a 10 year supply and many will not make it. A lot of would be flippers that bought these properties will not be happy with the results.

Low-income residents of the apartment complex moved, heavy construction equipment rolled in, millions of dollars were borrowed and dozens of investors saw double-digit returns on investments.

Now, all bets are off.

Lender USA Commercial Mortgage Co. and its related companies � better known as USA Capital � filed for Chapter 11 bankruptcy protection in Nevada on April 14. The filing follows a Securities and Exchange Commission investigation of how the company and its affiliates financed construction projects.

"Up until last week, we had no inkling that anything was wrong," said Virgil Birgen of Nevada, who, with his wife, invested $150,000 to build Sail Club at Clear Lake.

About 200 people from across the country gave Nevada-based USA Capital or a sister company money to fund the four-tower, 590-unit luxury high-rise on Executive Center Drive.

"We have always gotten paid," said an investor in the local property who asked that her name not be used. But when she recently asked to withdraw her $100,000, there were weeks of delays. Then the company went into bankruptcy court.

"I didn't get anything back," she said.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

A Look at Hyperinflation

Lately I see many people pointing to this that and everything else but especially rising home prices, gasoline prices, and commodity prices as if those constituted "hyperinflation". It is a word being bandied about without anyone having a firm grasp as to what it really means. Hyperinflation involves a complete and sustained collapse of faith in currency.

If you want to understand hyperinflation please look at Zimbabwe.

Back in the US, gasoline prices soaring 100% in response to peak oil has nothing to do with hyperinflation. In fact, soaring oil because of "peak oil" has nothing to do with inflation at all.

Oil soaring because of loose monetary policy does have something to do with inflation. Unfortunately it is very hard to see the difference.

Yet it is critical to understand the difference.

Please review:

In case you do not believe me or Saville perhaps you might believe Marc Faber. Please consider the article Marc Faber shatters prevailing market myths.

Yes, you can complain about medical prices, property values etc. But... If you have lived in your house for the last 5 years your expenses have gone down (assuming you were smart and refinanced anywhere close to the bottom). You can also complain about car prices but that will fall on deaf ears. We bought a brand new and very well equipped Hyundai Elantra (in 2005) for $10,500. Anyone paying $30,000 or whatever for an SUV and is now complaining about insurance costs and gasoline prices was simply asking for trouble in the first place.

Speaking of gasoline prices.......

The US has some of the lowest gasoline prices in the world.

'

'

Is that hyperinflation? Where?

To the extent that those prices are rising because of peak oil and not loose monetary policy, gas price hikes are not even a symptom of inflation at all.

Please do not mistake this post to mean I believe the CPI. I do not. It seriously understates energy prices, medical prices, education costs, property taxes, and a whole slew of other things. But the bottom line is that any talk of hyperinflation in the US is seriously misguided.

As for me, I am waiting for a turn down in credit expansion which is what the focus should be on. The threat is not where everyone is looking, and I guarantee you everyone is looking at inflation running out of control. Flashback 2002: does anyone remember the deflation threat? That the FED is now concerned about inflation after 15 consecutive rate hikes smacks of the same wrong way thinking of the Fed in 2000.

The Fed is almost always fighting the wrong battle so I agree with Faber that it should be abolished. A return to the gold standard and elimination of fractional reserve lending is just what we need. It would be a very painful adjustment to make, but a serious adjustment is coming anyway. We may as well make it the right one.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

If you want to understand hyperinflation please look at Zimbabwe.

333,200% increases is (no ifs ands or buts) hyperinflation.The BBC is reporting that Public hospitals fees have gone up from Z$300 to between Z$800,000 and Z$1m (US$10) with immediate effect, the state-owned Herald newspaper reported. The costs of consultations, maternity services, surgery and intensive care are also increasing.

The 333,200% increases come a month after the government lifted a freeze on private health care charges.

Back in the US, gasoline prices soaring 100% in response to peak oil has nothing to do with hyperinflation. In fact, soaring oil because of "peak oil" has nothing to do with inflation at all.

Oil soaring because of loose monetary policy does have something to do with inflation. Unfortunately it is very hard to see the difference.

Yet it is critical to understand the difference.

Please review:

In case you do not believe me or Saville perhaps you might believe Marc Faber. Please consider the article Marc Faber shatters prevailing market myths.

Q: How important is it to understand the role of the Federal Reserve to understand the world economy?Point blank, if the US was anywhere close to hyperinflation, Centex and other builders would not be knocking off $100,000 on the prices of their houses. I would not be able to buy chicken legs at .49 a pound on sale. Round roast would not be $1.69 lb on sale. I bought several roasts and had the store make ground round for me, paying zero% extra for the service. I recently bought whole turkeys at .69 lb and turkey breasts at .99 lb. Over Easter I bought a butt ham for .98 lb. Center cut pork chops not on sale are $5.49 lb. Phooey. Who needs that? At least once a month they are on sale for $2.29 lb or less. Seriously we are talking 1970's prices. I know because I worked as assistant manager in a grocery store back then. Heck I have no idea how they can even raise chickens at .49 lb. If you know then please tell me!

A: I think it is very important to understand the fact that we have a central banking system where the central banks can indicate, theoretically drop dollar bills from Helicopters. You wont be able to do that because all American helicopters are in Iraq. But they can print money, that is a fact and they can flood the system with liquidity.

Then you have to find a measurement of inflation. We measure inflation by rise in money supply. It would be wrong to think that the inflation is just consumer price increases. Inflation is a loss of purchasing power of your currency, dollar or Rupee. It can manifest itself by rise in consumer price but it can also manifest itself by a loss of purchasing power of money against real estate, or against stocks and real estate.

Q: What is the public enemy No 1 in your book, would it be inflation, or deflation?

A: In my book public enemy No 1 are the central banks. I think the world will be much better off under a gold standard. Other than that, I think the asset inflation is much more dangerous than consumer price inflation because asset inflation is driven by a huge credit bubble. Then asset prices become very expensive and when asset prices go down it leads to recession. So the Central Banks will support asset prices and see to it that they keep on going up. So they will inflate more and more and eventually you will come to an economic collapse.

Yes, you can complain about medical prices, property values etc. But... If you have lived in your house for the last 5 years your expenses have gone down (assuming you were smart and refinanced anywhere close to the bottom). You can also complain about car prices but that will fall on deaf ears. We bought a brand new and very well equipped Hyundai Elantra (in 2005) for $10,500. Anyone paying $30,000 or whatever for an SUV and is now complaining about insurance costs and gasoline prices was simply asking for trouble in the first place.

Speaking of gasoline prices.......

The US has some of the lowest gasoline prices in the world.

'

'Is that hyperinflation? Where?

To the extent that those prices are rising because of peak oil and not loose monetary policy, gas price hikes are not even a symptom of inflation at all.

Please do not mistake this post to mean I believe the CPI. I do not. It seriously understates energy prices, medical prices, education costs, property taxes, and a whole slew of other things. But the bottom line is that any talk of hyperinflation in the US is seriously misguided.

As for me, I am waiting for a turn down in credit expansion which is what the focus should be on. The threat is not where everyone is looking, and I guarantee you everyone is looking at inflation running out of control. Flashback 2002: does anyone remember the deflation threat? That the FED is now concerned about inflation after 15 consecutive rate hikes smacks of the same wrong way thinking of the Fed in 2000.

The Fed is almost always fighting the wrong battle so I agree with Faber that it should be abolished. A return to the gold standard and elimination of fractional reserve lending is just what we need. It would be a very painful adjustment to make, but a serious adjustment is coming anyway. We may as well make it the right one.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Tuesday, April 25, 2006

Jane Jacobs, 1916-2006

Jane Jacobs, the author of the legendary and immensely influential book The Death and Life of Great American Cities (among numerous other titles) died today in Toronto at the age of 89.

To learn more about Jacobs, check out Michael Blowhard's recent brief history and an interview with James Howard Kunstler from 2001.

To learn more about Jacobs, check out Michael Blowhard's recent brief history and an interview with James Howard Kunstler from 2001.

Monday, April 24, 2006

Monday, Monday

My weekly page update:

M House in Nagoya, Japan by architecture w.

The updated book feature is The Beatles: The Biography, by Bob Spitz.

Some unrelated links for your enjoyment:

M House in Nagoya, Japan by architecture w.

The updated book feature is The Beatles: The Biography, by Bob Spitz.

Some unrelated links for your enjoyment:

What to do with Southpoint Park?

Young architects from around the world ponder the question. (via ArchNewsNow)

Urbanscapes

"Architectural Speculation :: Landscape Future :: Urban Morphosis" (added to sidebar under blogs::urban)

noticias arquitectura

Now also in blog form. (added to sidebar under blogs::architecture)

Canaries at the Periphery

Please consider the following chart.

Mish note: I can not read what the text says but if you can please send me a translation. Regardless of what the text says, however, the universal language of the chart makes it quite clear that whatever is happening is not pretty.

Enquiring minds may be interested to discover that the above chart happens to be a graph of the Saudi stock market.

The Financial Times is reporting the Saudi market plunges 8% more.

An Active Role

Interestingly enough, Reuters recently reported Central banks should be active in a crisis.

The typical question was something like this: "OK Mish what does any of the above have to do with 'Canaries at the Periphery'?"

Canaries

The answer of course is that problems start at the periphery then work their way towards the nucleus. That is simply the nature of the beast. Please consider Canaries in the Coal Mine.

Closer to home John Hussman is writing about Market Action and Information.

Our view is that the longer this grind up occurs in the face of rising interest rates, deteriorating fundamentals, and huge divergences, the deeper the resultant plunge. Rot is now chewing its way at the periphery. It's only a matter of time before rot works its way to the core.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/

Mish note: I can not read what the text says but if you can please send me a translation. Regardless of what the text says, however, the universal language of the chart makes it quite clear that whatever is happening is not pretty.

Enquiring minds may be interested to discover that the above chart happens to be a graph of the Saudi stock market.

The Financial Times is reporting the Saudi market plunges 8% more.