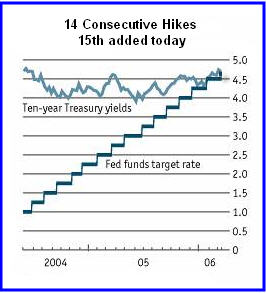

I am pleased to announce the start of a new club. It is called the Real Estate Apologists Club (REAC). There are no dues or fees or membership drives. One can not ask or apply for membership although one can indeed be granted a membership without asking! Furthermore, one can not opt out either. If the club chooses you, you are in, whether you like it or not.

Those worthy of membership are simply granted active membership. Those unworthy are banned as outcasts. That is all there is to it. I will give some specific examples later in this blog to help clarify the membership rules and hierarchy, but first it is time to show some nice charts created by my friend

Calculated Risk. The annotations and trendlines were added by me.

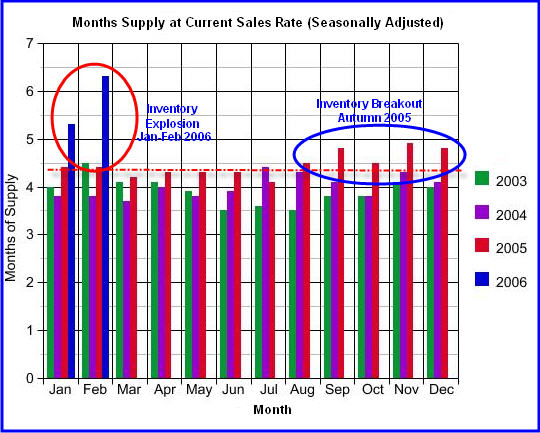

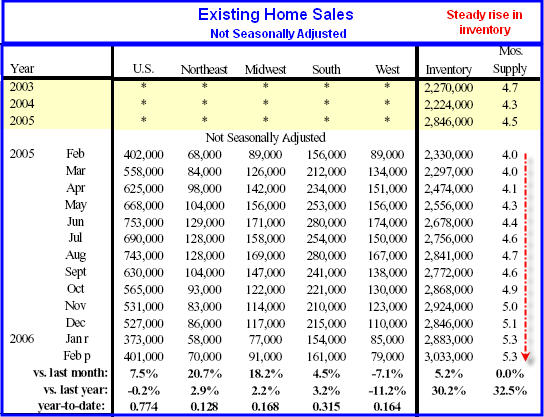

Click on any chart for an enhanced view of that chart.Current Housing Inventory

Notice how home inventories kept bumping up against the upper trendline for months. In Autumn of 2005, there was a trendline breakout followed by an inventory explosion in January and February of 2006.

Bear in mind that home builders are still building like mad.

Some even went on land buying sprees as late as last Autumn. Over the next few months that new inventory will be added to the existing supply. Note too that while sales have declined, they are still at very high levels. Should sales decline further the months inventory numbers could skyrocket.

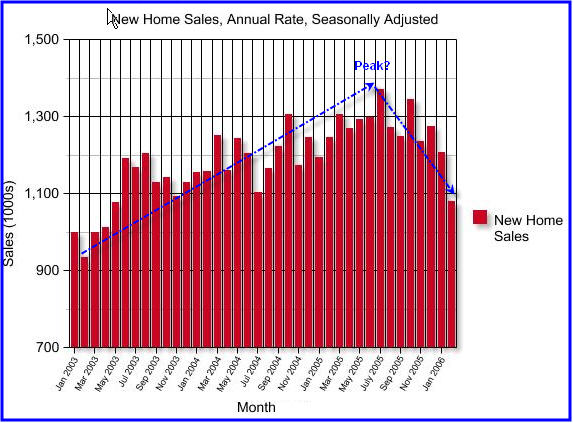

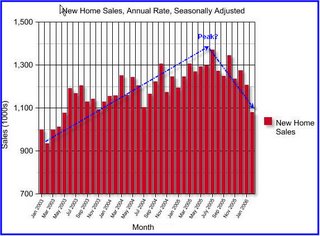

New Home Sales

This is yet another chart that only a true real estate believer could make excuses about.

Sales have been trending down ever since July.

There are no more stories about people camping out in Florida to get on a condo waiting list at absurd prices.

Florida, California, and other bubble areas have popped. Has that fazed any true blue believer in real estate one bit? Of course not and such people are likely card carrying REAC members.

REAC Admission PolicyOK Mish, who is in the club and who is out based on today's reporting?

Good question. Let's take a look:

The Financial Times is reporting

Signs of slowdown in US housing.

Sales of new US homes plunged 10.5 per cent last month, prices fell and the stock of unsold homes hit its highest level in 10 years, providing the clearest indications yet that the red-hot housing market may be cooling.

New home sales slid to 1.08m, the fourth consecutive decline, and the price of new homes fell 3 per cent from a year ago. With a flood of new properties coming on to the market, at the present pace of sales, it will take 6.3 months to clear the backlog.

Ian Morris, economist at HSBC, said: �Over the next 12 months we suspect a hard landing is more likely.�

Whoa. Stop right there. Any economist even admitting the possibility of a hard landing, let alone thinking one is "more likely", is not what we are looking for as a certified REAC member. Ian Morris, this is your one and only warning. Any further talk like that and a black mark will be placed on your soul barring you from ever being considered for admission to the REAC. Clearly we are looking for much sterner stuff that that, so we simply move on.

The Herald Tribune is reporting

Existing home sales drop, along with some pricesThe Florida real estate market is definitely showing signs of doing what many economists have long predicted: slacking off the feverish tempo of 2004 and '05 and getting back to normal.

One area where that is becoming more evident is pricing, which has so far been almost unshakable bedrock in Southwest Florida's real estate market.

Though February's year-over-year median sales prices in the Sarasota and Charlotte County-North Port markets remained in the double digits -- 24 percent and 20 percent, respectively -- a report from the Florida Association of Realtors showed clear pricing pressures.

Bravo Realty's Thomas Heimann stands by his earlier bearish prediction of a 20 percent "price correction" this year.

Any predictions of 20% price corrections are pure blasphemy. There can be no warnings given for such outrageous talk. Thomas Heimann, a black mark has been placed on your soul and you must now pray to the REAC Pope for special dispensation.

The Palm Beach Post is reporting

Home sales slow, prices dip.

The typical price of a house in Palm Beach County dipped for the third month in a row as the housing market continued its return to reality.

The median price for an existing single-family home sold in February was $391,000, the Florida Association of Realtors said Thursday. That's down slightly from January and well below November's peak of $421,500.

"We're not in a bust; we're in the middle of a correction," said Douglas Rill, a longtime broker and owner of the 140-agent Century 21 America's Choice in West Palm Beach. "That frenzied 2005 market is over."

The shift is a healthy one, said Kiku Martinson, director of real estate at Campbell & Rosemurgy, a 120-agent brokerage with offices in Boca Raton and Deerfield Beach.

"This is a better market for everyone," Martinson said. "We don't have the craziness that we had, where buyers had to make an offer right away. It's a little bit more relaxed, and buyers can study their options."

Still, many Realtors insist the slowdown is nothing more than a myth created by the media. Christian Angle, an agent at Earl A. Hollis Inc. in Palm Beach, said homes that are "priced right" are still selling.

"The market is very strong," Angle said. "My phone is ringing off the hook."

Ding Ding Ding, we have two "winners".

I am sorry Mr. Rill, you are not one of them. Your no-bust position is admirable of course,

"We're not in a bust; we're in the middle of a correction" but talk of "corrections" are just too wishy washy right now. If you do not have a single sale for 6 months and then repeat your statement, we will place you back into consideration. For now, the REAC is looking for much sterner stuff.

This is more like it:

The shift is a healthy one, said Kiku Martinson, director of real estate at Campbell & Rosemurgy, a 120-agent brokerage with offices in Boca Raton and Deerfield Beach. "This is a better market for everyone".Wow! That is the kind of stern stuff we are looking for. Welcome to the club, Kiku.

We are also ringing the club inclusion bell for Christian Angle. "

The market is very strong," Angle said. "My phone is ringing off the hook." The Palm Beach Post is also reporting

Potential foreclosures climb as housing market cools.

There's trouble in the bubble.

After three years of rapidly inflating real estate, loose credit and dicey financing, the number of court filings notifying Palm Beach County property owners they are facing foreclosure is rising.

Martin County's pre-foreclosure filings are at their highest level since February 2005, and in St. Lucie County 113 pre-foreclosure notices were filed between Jan. 1 and March 23.

The Palm Beach County numbers are not huge. February's 159 pre-foreclosure filings fall well below February 2005's 192.

But they represent a 34 percent hike from October, when the increase began.

"That is a trend, not a blip," said Jack McCabe, chief executive of McCabe Research and Consulting in Deerfield Beach, adding that too many good people took out too many bad loans.

I have been following this McCabe character for quite some time. He has a double black mark on his soul. That makes him ineligible for a

plenary indulgence at any time in the future. He is forever banned from the REAC just as Pete Rose is from Baseball's Hall of Fame.

Triple black mark outcasts at this time include the evil Rich Toscano aka

Professor Piggington, Patrick Killelea at

Patrick.Net, Ben Jones at

TheHousingBubbleBlog.Com and Robert Campbell at

RealEstateTiming. Additional names will be added as appropriate.

The California Association of Realtors is reporting

California Sales �Plunge�, Inventory At Multi-Year High

California Sales �Plunge�, Inventory At Multi-Year High�Existing-home sales dropped significantly in California in February, falling 15.5 percent from the same period a year ago, as inventory levels climbed and median prices continued to escalate, an industry trade group reported today. Meanwhile, the February 2006 median price of an existing home in the state decreased 2.9 percent compared with January�s $551,300 median price.�

The state�s builders think the solution is more construction. ��We may be producing some of America�s best college graduates, but we�re exporting them to states where owning a home is more than just a fantasy,� said Alan Nevin, chief economist at the California Building Industry Association. The state�s 57 percent homeownership rate, the second lowest behind New York, lags far behind the national average of nearly 70 percent.�

Ding Ding Ding. We have another winner.

Alan Nevin, welcome to REAC. Anyone that thinks the solution to high inventory is more building and more condos is clearly a candidate for the REAC upper hierarchy. Perhaps Mr. Nevin would make a good Bishop.

I have two questions for Mr. Nevin:

1) If extra supply lowers prices as the CBIA suggests, how do prices not drop?

2) True believers think that housing prices will never drop, so why did median price drop 2.9% now year over year and how do you explain #1?

If those questions can be properly explained or avoided by Mr. Nevin, then he is eligible for promotion to Cardinal. A Papal candidate, however, would never put himself into such a tough predicament. We must look further to find the Pope of the REAC.

The Baltimore Sun is reporting

New home sales drop by 10.5%.

"The new home market looks like it is starting to stagger," said Joel Naroff, chief economist at Naroff Economic Advisers, a Pennsylvania forecasting firm. "Bubbles do burst, they really do."

David Seiders, chief economist for the National Association of Home Builders, said he still believes that sales of new homes will post a moderate decline of around 8 percent this year, with home price gains slowing from double-digit increases of around 12 percent to about half that level.

Ding Ding Ding. Welcome to the club David Seinders, and a pox on your soul Mr. Naroff.

In a quote that I can not now find via Google search, but nonetheless I am positive I recorded accurately earlier today, I must ring the bell for

Ian Shepherdson chief US economist at High Frequency Economics who described the figures as "awful" but said they did not yet provide convincing evidence of a collapse. "One bad month is not a trend, and sales may have been hit mid-month by the record snowstorm on the Atlantic seaboard." he said.

We had the third best Winter weather in recorded history and he is blaming a "mid-month snowstorm"? That is just what is needed for the REAC hierarchy: creative attacking thinking no matter how wrong that thinking is. Unfortunately he used the word "awful". That I am afraid is a no-no.

We are still ringing the bell, however, for his creative thought processes, yet we must caution Mr. Shepherdson for the obvious flaws in his thinking.

Highest praise and certain cardinalship would have been awarded for a statement like this:

"Sales are extremely good given the mid-month record snowstorm on the Atlantic seaboard. One bad month is not a trend. Naysayers will be proven wrong just as they have for the last 32 years. A rebound can be expected anytime soon and smart buyers will be snapping up these bargains now ahead of the crowd. This is a good market for everyone. There has never been a better time to buy than now. They do not make land anymore and they never will again."Repeated statements like the above, with no intermittent slips or mistakes, would make one eligible for Popedom, and then REAC sainthood. As for now, the search continues.

OK enough silliness.

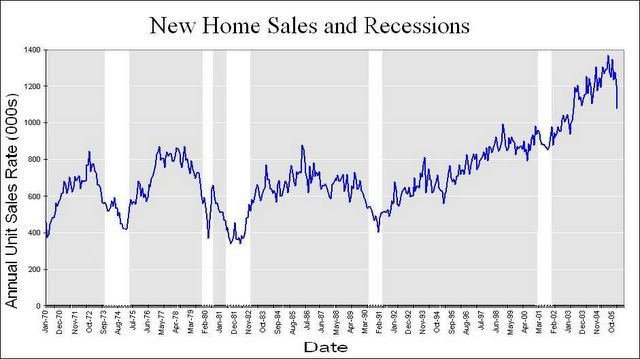

Calculated Risk put out one more chart today and gave me permission to share it.

New Home Sales vs. Recessions

Anyone that fails to understand the significance of the above charts is likely to become a card carrying member of REAC. A real estate bust and recession are both coming our way.

Mish note: No offense is meant nor should any be taken by anyone of any religious faith. I used Catholic hierarchy analogies for this post only because I am familiar with them by upbringing. This was an attempt to poke fun at "The Apologists Club", no more no less, using ideas that I could easily relate to from personal experience.

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/