Toll Brothers, Meritage Homes and Simon Property Group Joint Venture

announce the purchase of a 5,485-acre land parcel in Phoenix's Northwest Valley for $312 Million.

It is the largest real estate transaction in Arizona history.

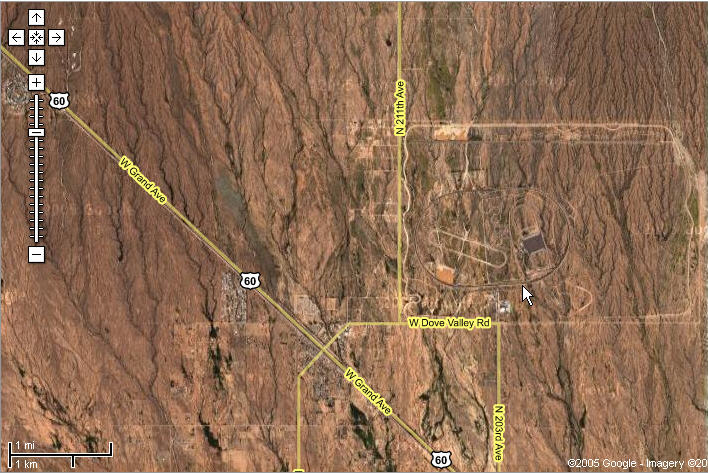

The Maricopa County property, which DaimlerChrysler currently utilizes as a vehicle endurance testing and development facility, is bound by 183rd Avenue on the east, 211th Avenue on the west, Dove Valley on the south and Joy Ranch Road on the north. DaimlerChrysler will continue to lease the property for the next few years, in order to plan and accommodate for the orderly transition of its testing operations.

Toll Brothers and Meritage Homes each plan to build a significant number of homes on the site. Simon Property Group, Inc. has the option to purchase a substantial portion of the commercial property. Other parcels may be sold to third parties. Initial plans call for a mixed-use master planned community, which will include approximately 4,840 acres of single-family homes and attached homes. Approximately 645 acres of commercial and retail development will include schools, community amenities and open space. Initial homes sales are tentatively scheduled to begin in 2009. According to the approved General Plan, the site allows between 15,000 to 31,000 homes.

Robert I. Toll, chairman and chief executive officer of Toll Brothers, Inc., stated: "We are thrilled to have been chosen by DaimlerChrysler and to have teamed up with two excellent partners to develop this fabulous piece of real estate. The northwest area of Phoenix has experienced unprecedented popularity and this particular parcel is a highly coveted site."

$312 million for 5,485 acres of desert with a testing track on it. That amounts to $56,882 dollars per acre of flat desert.

Enquiring Mish bloggers might be wondering exactly where "Phoenix's Magnificent Northwest Valley" is. Thru the wonder of Google satellite imagery I am pleased to show everyone the following pictures of just what that consortium of buyers got for their $312 million.

Here is this "highly coveted site".

It seems to be about 35 or 40 miles away from Phoenix.

The attraction? A commute from there to downtown during rush hour might be close to an hour each way and where will gas prices be in a couple of years anyway?

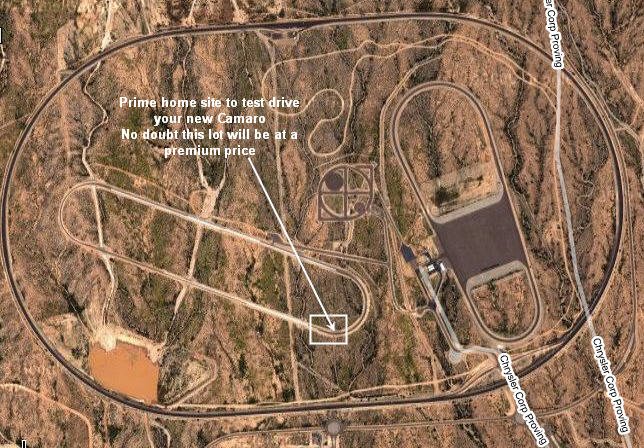

Let's zoom in looking for the attraction.

I do not see any do you?

Let's zoom in further.

There it is. I boxed it in. The premier spot to test drive your new Camaro, provided of course Toll Brothers decides to keep that test track up and running. If not, what the attraction?

Homebuilders Buried in LandWith that in mind, I note with interest this Street.Com article entitled

Homebuilders Buried in Land. Enquiring Mish readers might want to know more so let's take a look at that too.

Ed Wachenheim, a long-term value investor, agrees with the general view that homebuilder stocks are cheap right now. But the money manager, who was once a major owner of the sector, has sold off most of his positions because he's worried about the huge amount of land on builders' books.

"My fear is that many of the companies took on too-large land positions at too-high prices. And that means that should the industry turn down that there is risk that there will be some impairment of land values," says Wachenheim, who runs Greenhaven Associates, a Purchase, N.Y.-based firm that manages $3.7 billion of capital, mostly for wealthy individuals.

It's difficult to determine if Wachenheim's concerns are justified and builders have been too aggressive in taking on new land. Builders report the dollar value of their total land holdings in quarterly filings, but nothing is usually said about the prices paid for individual parcels.

There also is no geographic breakdown to determine whether a builder like Pulte Homes has too much exposure to a frothy market like Las Vegas. All the public knows is that Pulte's total inventory of owned land was $5.3 billion for the quarter ending Sept. 30, up from $4.49 billion a year earlier. That amounts to 170,000 home lots, or roughly three years of supply, the company says.

But what if that's too much land to be holding in a slowing housing market?

The issue is of particular note since builders have spent the bulk of their earnings over the past few years buying land for future building. Although most builders have at least 50% of their lots controlled through options, a large amount of purchased land continues to be placed on balance sheets. As a result, the sector in general has seen negative cash flows for some time now.

"I have never seen a group, in 20 years of analysis, post negative cash flow from earnings for four of the last five years and prosper as a stock group without having to pay the piper," says Jim Poyner, an analyst for Palladian Research, an independent New York research house. Poyner thinks land impairments could begin popping up over the next year if builders start slashing prices on new homes for sale.

Robert Curran, a Fitch Ratings analyst who covers the builders, says it's premature to worry about land impairments now, but grants that the issue could arise in the future.

"There isn't anyone who really stands out as being overloaded on raw land on the balance sheet that is just sitting there," Curran says. It would take an economic recession or a really problematic regional housing market for there to be large land impairments, he adds. "If home prices come down, it doesn't mean you will write down land assets."

Another Telepathic QuestionOn that thought I just received another telepathic question. It's been a while since we have had one of those and here it is:

"But Mish what about those fabulous PEs?"Those PEs are a mirage. The homebuilders have negative cash flow and keep sinking every penny of their earnings into land, land, and more land at increasingly absurd prices as the article above addressed, and that transaction proved.

Here is the homebuilder picture:

- Homebuilders have negative cash flows

- Homebuilders put the bulk of their profits into buying more land at absurd prices

- Homebuilders are totally ignoring the yield curve

- Homebuilders are discounting the odds of a recession

That of course does not mean that homebuilders will sink anytime soon. They may or they may not. There has been one hell of a short squeeze lately and everyone seems to be playing the trend of 2003 right now. No one seems to see falling sales, rising inventories, sinking refis, and discounts by the home builders.

Just two weeks ago I was told by a Real Estate Broker friend of mine that Atlanta was impervious to a slowdown and there would be no recession coming our way. I note with interest

This ad by Centrex.

$60,000 off?

Everything is fine in Atlanta?

Everyone seems to think their area is impervious to a slowdown because of demographics, warm weather, an ocean, or whatever. That seems to be the key to this mania.

Well I have news for you.

An

Interest Rate Squeeze does not care where you live. Prices matter as do prevailing rents. Home prices do not always go up. Please click on that link and see what I am talking about. I suspect Toll Brothers and Meritage Homes will find out in due time just how silly that purchase in Phoenix was. By then it will be too late. It is the overpayment for land that bankrupts homebuilders every cycle. This cycle will be no different.

Mish note: This article originally appeared in

Whiskey and Gunpowder.

Following are three comments I received in response to that publication:

From: Connie

Subject: Phoenix real estate - I live here!!

I live in the east valley of Phoenix, and I can tell you things are really slowing down here, as existing homes are sitting unsold for weeks now and prices are dropping. I am planning to leave the area soon because there will not be any water here in the coming years and it will be a MAMMOTH problem. No one seems to care now but it is coming! I have been called numerous times to come to an opening of Dell Webb new project. I think they are having trouble getting interest in it and they keep saying they "haven't decided on prices yet" so what's up with that? Keep up the good work,

C.J. Phoenix, AZ

==================================================

Subject: $312 million for that?

Why buy land for housing development? They should've invested in a tract of mineral rich land in Nevada. At least when the housing market implodes they could start mining for gold, or sell it on to one of the big resource hungry blue chips. Or is there actually precious yellow metal under that ground they purchased near Phoenix that no-one is aware of?

Regards,

J.N.

==================================================

Subject: Phoenix Desert

Hi There,

You missed a major point. Where are they going to get the water for all those houses? The Colorado River is over subscribed. One of the worst droughts in history is going on there in Arizona right now. And those of us up here in the Rust Belt just cemented a deal so they cannot steal water from the Great Lakes. Oh well, in 20 years it will all be part of Mexico once again, anyway.

Keep up the great work!

S.B.

==================================================

Mike Shedlock / Mish

http://globaleconomicanalysis.blogspot.com/